Executive Summary

Advanced depreciation mechanisms, notably bonus depreciation and Section 179 expensing, have long served as pivotal tools for U.S. businesses to accelerate tax deductions on capital investments. The Tax Cuts and Jobs Act (TCJA) of 2017 introduced 100% bonus depreciation, allowing businesses to deduct the full cost of qualifying assets in the year they were placed in service. However, this provision is undergoing a phased reduction, with significant implications for industries such as real estate, oil and gas, and manufacturing.

What You Need to Know Right Away

If you run a business and buy equipment, software, or invest in property—this tax strategy can save you serious money. It’s called advanced depreciation, and it lets you write off big purchases much faster than usual, cutting your tax bill significantly.

But here’s the thing: The rules are changing, fast. What was 100% deductible is now dropping to 40% in 2025—and may disappear completely by 2027 unless Congress acts.

This guide will show you:

What advanced depreciation really is

What’s changing and when

Who benefits most

How you can take advantage of it right now

Understanding Advanced Depreciation

Bonus Depreciation

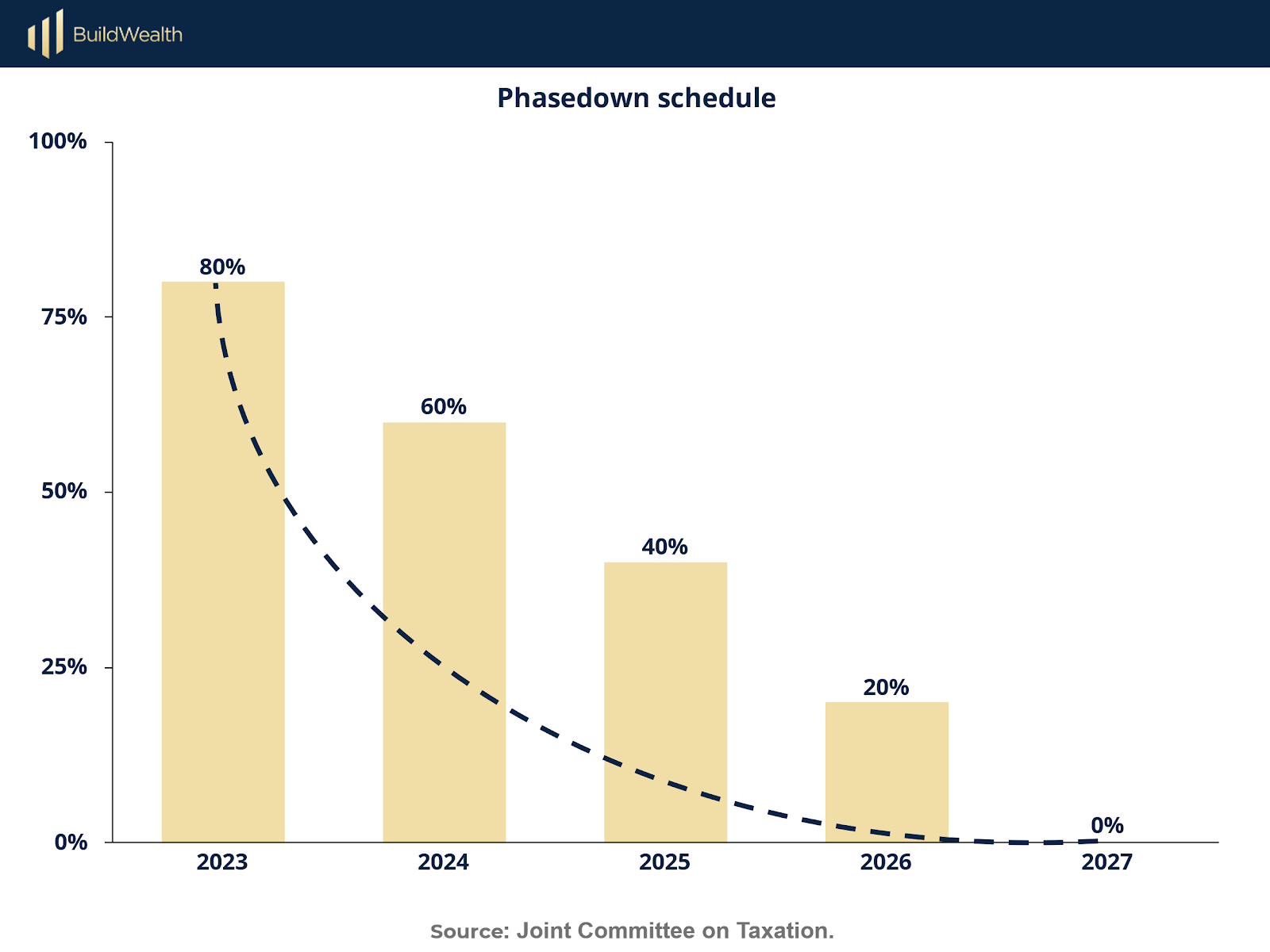

Bonus depreciation permits businesses to immediately deduct a significant percentage of the purchase price of eligible assets. The Tax Cuts and Jobs Act (TCJA) of 2017 introduced a 100% bonus depreciation allowance for qualifying machinery and equipment purchases made between 2018 and 2022. Beginning in 2023, the deduction is scheduled to phase out in 20-percentage-point increments annually, reaching 0% by 2027.

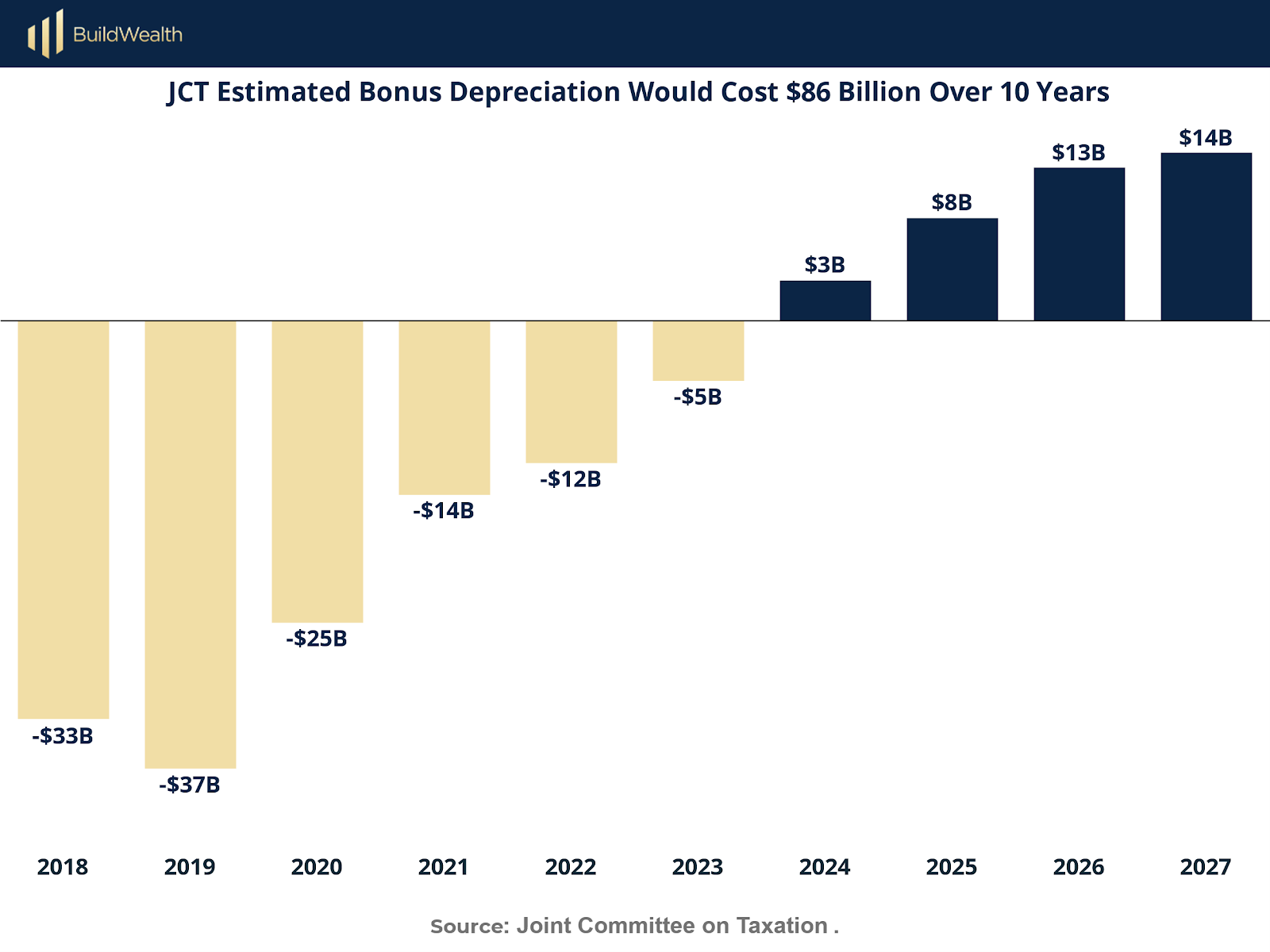

According to a 2017 estimate by the Joint Committee on Taxation (JCT), this provision was projected to cost $86 billion for the government, over a decade. However, part of that figure reflects anticipated increases in federal revenue from 2024 to 2027, as businesses were expected to accelerate their capital investments and claim deductions earlier in the period.

The phasedown schedule is as follows:

This phasedown impacts the immediate tax benefits businesses can realize from capital investments, necessitating strategic planning to optimize deductions.

Who Pays the $86B+ Cost?

Great question. When we say "this costs $86 billion," that’s not your cost—it’s the estimated reduction in federal tax revenue over 10 years. In other words, the IRS collects less because businesses like yours pay less in taxes.

This isn’t government spending—it’s the government letting you keep more of your money now, to reinvest in your growth.

Why Should I Care?

Because:

You’re leaving money on the table if you don’t use these deductions.

They reduce your taxable income, which lowers what you owe.

You can reinvest that money into growth—equipment, hiring, expansion.

In fact, the Tax Foundation estimates permanent 100% bonus depreciation could:

Grow U.S. GDP by 0.5%

Add 85,000+ jobs nationwide

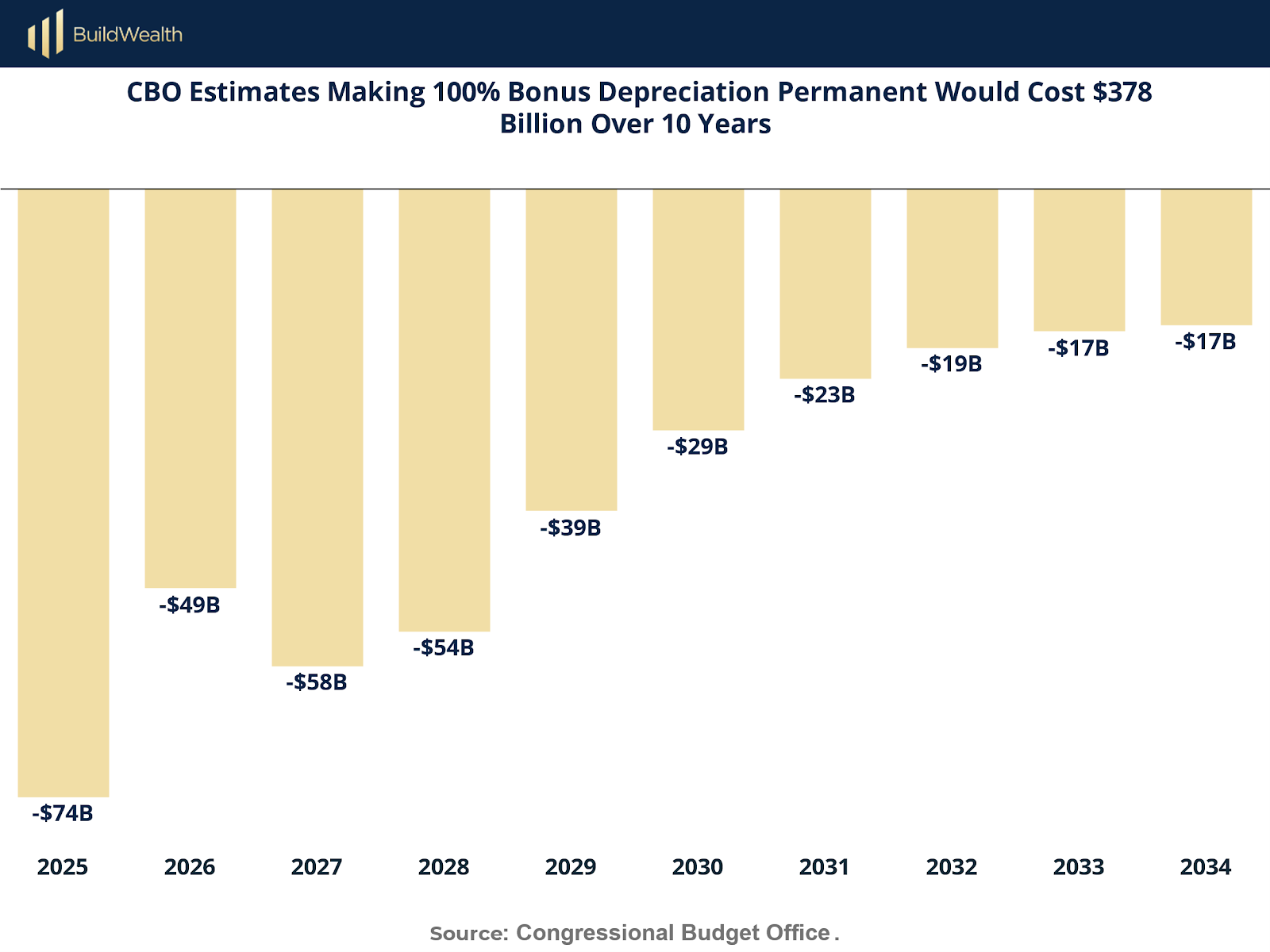

The Congressional Budget Office (CBO) projects that extending 100% bonus depreciation over the next decade would cost approximately $378 billion, with nearly 75% of that expense concentrated in the first five years. While maintaining or reinstating pro-growth tax policies is essential, it is equally important to ensure that any new tax cuts or spending increases are responsibly offset to prevent ballooning deficits from undercutting the intended economic benefits.

According to economists and policy analysts, making bonus depreciation permanent would likely boost the U.S. economy by encouraging greater investment in machinery and equipment—key drivers of productivity and, consequently, economic growth.

The Tax Foundation estimates that 100% bonus depreciation would raise long-term GDP by 0.5% and generate more than 85,000 jobs. Similarly, analyses by the Penn Wharton Budget Model and the Joint Committee on Taxation (JCT) conclude that the policy would lead to increased business investment and stronger GDP growth.

Section 179 Expensing

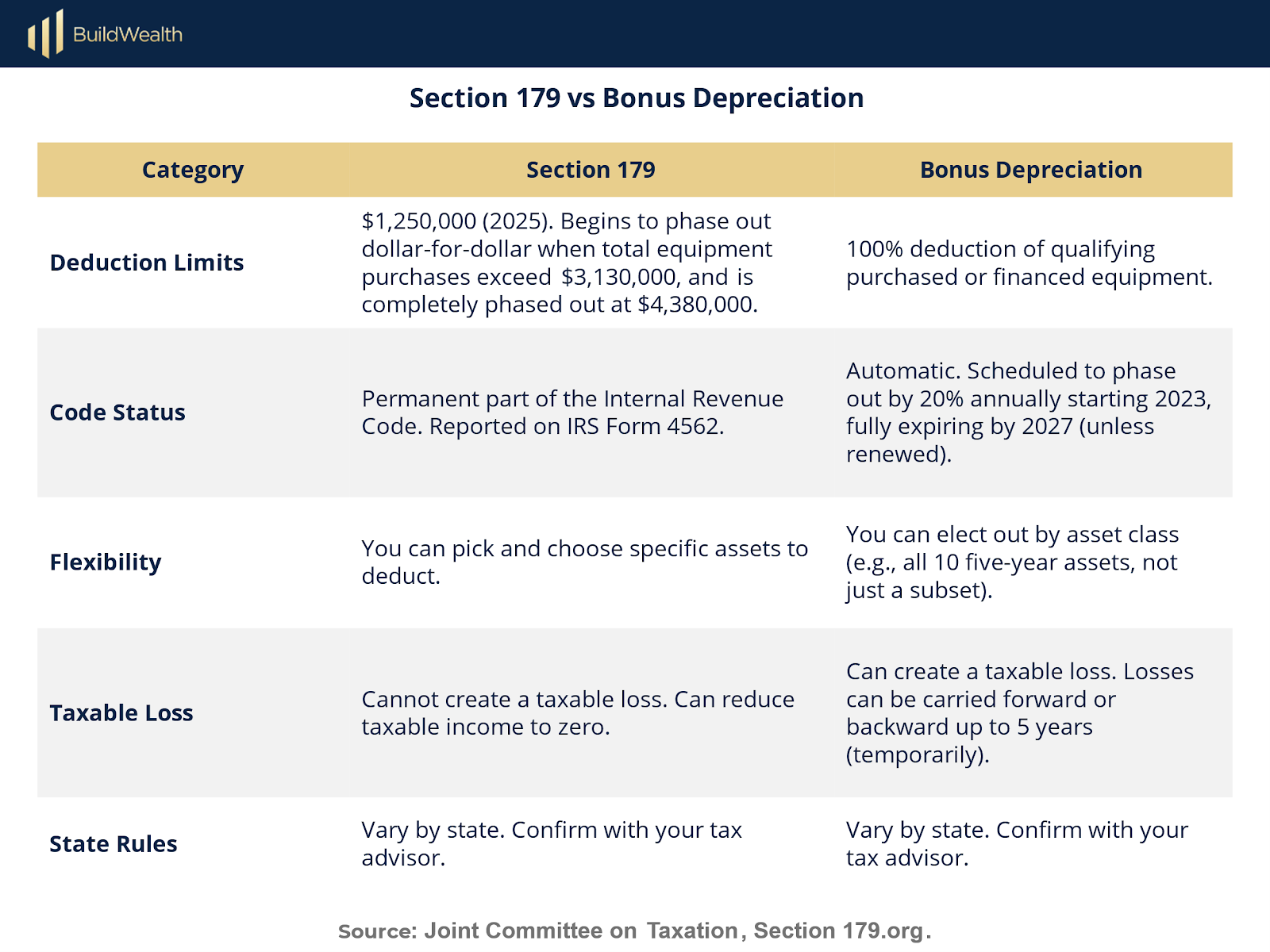

Section 179 allows businesses to deduct the full purchase price of qualifying equipment and software purchased or financed during the tax year. For 2025, the deduction limit is $1,250,000, with a phase-out threshold of $3,130,000. These limits are indexed for inflation and may see slight increases in subsequent years.

Unlike bonus depreciation, Section 179 expensing is limited to taxable income, meaning businesses cannot use it to create a net loss. However, it offers flexibility in selecting specific assets for expensing, allowing businesses to tailor their depreciation strategies.

Section 179 vs. Bonus Depreciation: How to Use Both

Section 179 Expensing:

Deducts up to $1.25M of equipment costs

Begins phasing out if you spend more than $3.13M

Applies to new or used assets

Can’t reduce income below zero

Bonus Depreciation:

Covers the remaining balance

No cap on how much you can deduct

Can create a tax loss (useful if you need to offset other income)

Use both together. You apply Section 179 first, then bonus depreciation picks up the rest.

Here’s why combining both may be advantageous:

1. Section 179 alone offers limited benefits in certain cases.

The Section 179 deduction, along with its phase-out threshold—set at $1,250,000 and $3,130,000 respectively for tax year 2025—are now permanent features of the tax code. However, because bonus depreciation now applies to both new and used assets, Section 179 tends to be most useful in more specific business situations, such as for smaller capital purchases or for businesses seeking to control taxable income more precisely.

2. Bonus depreciation is on the decline.

With the bonus depreciation rate dropping to 40% in 2025 and scheduled to decrease further in the following years, businesses are incentivized to invest in equipment sooner rather than later to take full advantage of the remaining benefits.

3. Eligible property includes more than just machinery.

Qualifying assets also include off-the-shelf software, meaning even businesses that aren’t investing in heavy machinery can leverage these deductions. It's also worth noting that if total equipment purchases exceed $4,380,000 in 2025, the Section 179 deduction phases out entirely—though bonus depreciation may still apply to the excess amount.

Who Wins Big?

Real Estate Investors:

Deduct interior improvements (QIP) faster

Use cost segregation to break buildings into faster-depreciating parts

Maximize tax shelter early

Oil & Gas:

Front-load expensing of drilling and infrastructure costs

Offset high upfront costs from exploration and development

Manufacturers:

Deduct machinery, tools, and automation tech

Offset income and reinvest in production

New Law in Play?

Congress is considering a law (TRAFWA) to extend 100% bonus depreciation through 2025, but it’s not final yet. As it stands, the deduction drops to 40% next year.

Be prepared, but don’t count on Washington. Act based on what’s certain today.

What Should You Do?

Here’s your decision checklist:

If you plan to buy equipment or software: Make the purchase before December 31, 2025 to claim 40% bonus depreciation or more.

Spending less than $1.25M? Section 179 might fully cover you. Easy win.

Spending more than $3.13M? Use bonus depreciation for the rest—it has no cap.

Real estate investment? Use a cost segregation study + bonus depreciation to increase early write-offs.

Unsure how this applies? Speak to your accountant now—waiting could cost you thousands.

Strategic Considerations

Asset Acquisition Timing: Businesses may consider advancing capital purchases to capitalize on higher bonus depreciation rates before further reductions.

Cost Segregation Studies: Particularly in real estate, cost segregation can identify assets eligible for shorter depreciation lives, maximizing deductions.

Section 179 vs. Bonus Depreciation: Evaluating the interplay between Section 179 expensing and bonus depreciation can optimize tax outcomes, especially considering limitations and thresholds.

Legislative Monitoring: Staying informed on potential legislative changes is crucial, as extensions or modifications to depreciation provisions can significantly impact tax planning.

Conclusion

You don’t need to be a tax expert to take advantage of advanced depreciation. But you do need to act.

Waiting until the rules change—or worse, expire—means smaller deductions and higher taxes.

Be proactive. Be strategic. And talk to your tax advisor now.

Premium Perks

Since you are an Wealth Stack Subscriber, you get access to all the full length reports our research team makes every week. Interested in learning all the hard data behind the article? If so, this report is just for you.

Want to check the other reports? Access the Report Repository here.