In a private capital landscape reshaped by higher rates, extended holding periods, and shifting liquidity demands, secondaries have gone from niche strategy to necessary infrastructure. From trade sales and IPOs to continuation funds and NAV-based financing, GPs and LPs alike are recalibrating their approaches to liquidity, and secondaries are leading that evolution.

This report explores the data behind that shift. What you’ll see is a maturing market that’s not just growing, it’s innovative. Transaction volumes are hitting record highs, dry powder is abundant and increasingly efficient, and new structures like continuation funds are offering sponsors and investors alike more control, more flexibility, and more strategic options than ever before.

If you’ve heard the buzz about secondaries but haven’t yet considered how they fit into your capital allocation strategy, now’s the time to look closer.

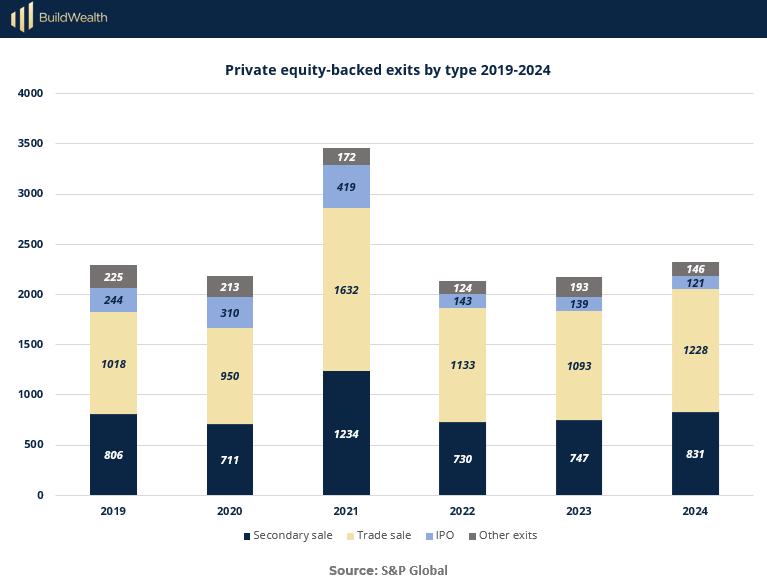

A Rebound in Exits, and the Steady Role of Secondaries

After a dramatic spike in 2021, private equity-backed exits slowed significantly in 2022 and 2023 due to macroeconomic headwinds, deal-making uncertainty, and tightened capital markets. But now, early 2024 figures point to a rebound in activity, particularly in secondary sales and trade sales.

This resurgence suggests improving market confidence and a return to more normalized exit conditions. While IPOs remain muted compared to their 2021 peak, their stabilization alongside other exits hints at a rebalancing in how GPs are approaching liquidity.

What stands out in this chart is the consistent role of secondary sales across all the years, even during periods of market stress. In fact, secondaries have grown again in 2024 to 831 transactions, recovering toward 2021 levels.

This consistency reinforces the idea that secondaries are not just an alternative, they’re a core component of exit planning. As PE firms adapt to a more selective exit environment, secondary sales offer a controlled, flexible pathway that is proving indispensable across market cycles.

Strategic Investor Takeaways:

2024 Exit Recovery Is Underway: Early signs show exit activity—especially trade and secondary sales—trending up again, offering renewed confidence for capital recycling.

Secondaries Are the Reliable Constant: Through boom, bust, and bounce-back, secondaries have remained a stable exit option—underscoring their resilience and strategic utility.

IPO Volumes Are Still Subdued: While public markets have steadied, IPOs remain well below peak levels, reinforcing the need for diversified liquidity strategies.

Trade Sales Regain Momentum: The resurgence in trade sales (now at 1,228 in 2024) suggests strategic buyers are re-entering the market, but secondaries remain crucial where sales aren’t feasible.

Forward-Looking Portfolios Will Prioritize Flexibility: Investors allocating to private markets need to consider the role of secondaries not just for liquidity, but as a way to manage exposure and reduce reliance on single-exit events.

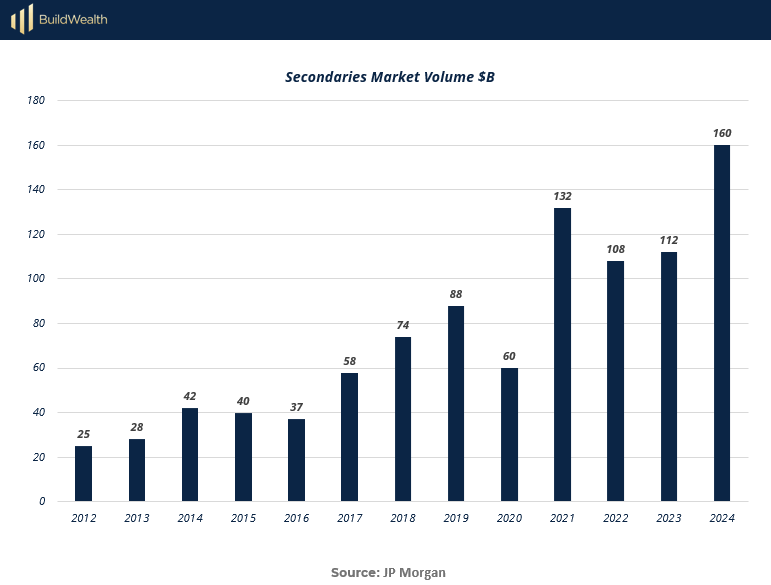

The Rise of the Secondaries Market: From Niche to Necessity

After several years of steady growth, the secondaries market has entered a new phase. In 2024, transaction volume reached a record $160 billion—well above the prior high of $132 billion in 2021. This surge isn’t a fluke; it’s the product of a structural shift. As private market assets continue to age and liquidity needs mount, institutional investors are increasingly turning to secondaries as a core portfolio tool rather than a tactical solution. What once lived in the background of private markets is now moving to the front of the stage.

This leap in volume reflects rising comfort with secondary transactions across the board: from LP-led portfolio sales to increasingly sophisticated GP-led deals. Market participants are no longer just “testing the waters”—they’re scaling in. The growth also coincides with broader private equity dynamics: longer hold periods, greater NAV transparency, and more innovative deal structures. If 2021 proved the potential of secondaries, then 2024 confirms their staying power and strategic importance.

Key Takeaways for Investors:

New Record Volume ($160B): 2024 marks the highest-ever transaction volume, underscoring the secondaries market’s maturity and momentum.

Acceleration, Not Just Recovery: The post-2021 pullback has been decisively reversed. This isn’t just a rebound—it’s a breakout.

Widening Adoption Across LPs and GPs: From pensions to family offices, more players are using secondaries proactively to manage exposure, liquidity, and portfolio construction.

Signals Institutional Confidence: Large-scale volume increases indicate strong buy-side appetite and a deepening pool of willing sellers—both signs of a healthy, liquid marketplace.

Timing Matters: For investors considering secondaries, entering during a volume upswing means access to more deal flow, competitive pricing, and enhanced diversification opportunities.

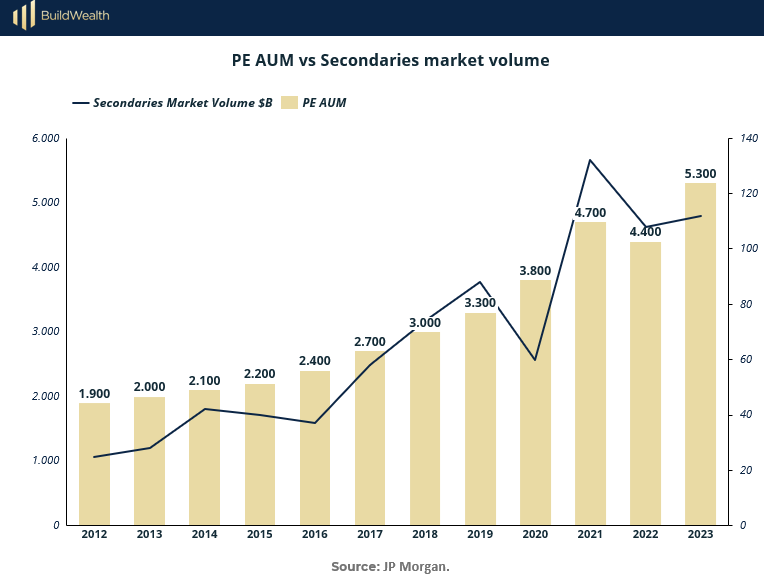

Growing Private Equity AUM Sets the Stage for Secondaries

Private equity as an asset class has undergone tremendous growth over the past decade. Assets under management (AUM) have nearly tripled, rising from $1.9 trillion in 2012 to a staggering $5.3 trillion by 2023. As allocations to PE have surged, so too has the need for liquidity options, especially as traditional exit paths become more constrained.

This is where secondaries are stepping into the spotlight. As the orange line in the chart shows, secondary market volume has scaled up in lockstep with AUM, reflecting how central this once-niche market has become to managing exposure in a maturing private capital landscape.

What’s striking is that while AUM has grown steadily, secondary volume has increased even faster in recent years, particularly since 2020. This divergence suggests that investors are no longer viewing secondaries as reactive tools, but as proactive components of portfolio strategy.

As more capital gets locked into longer-dated vehicles, and as GPs look for creative ways to return capital without selling high-conviction assets, secondaries offer the kind of agility and innovation that traditional private equity structures lack. For any executive to evaluate how to build smarter exposure to alternatives, understanding this relationship between PE AUM and secondaries is essential.

Key Investor Takeaways:

Massive PE Growth Fuels Demand for Liquidity: With PE AUM surpassing $5 trillion, institutional investors need mechanisms to adjust and manage positions—especially when exit timelines stretch.

Secondaries Are Scaling Faster Than AUM: The secondary market has grown disproportionately, signaling that its use is becoming more mainstream and strategic, not just situational.

Liquidity Is the New Alpha: In an environment where holding periods are extending, access to liquidity without sacrificing exposure is becoming a competitive edge for LPs.

Alignment With Long-Term Portfolio Construction: Secondaries are helping investors maintain or reshape their private equity allocations without having to enter or exit full fund cycles—adding control and precision to allocation strategies.

Indicator of Market Maturity: The rise of secondaries relative to AUM suggests that private equity, as a market, is entering a more flexible, sophisticated phase—one that favors investors who understand and can navigate liquidity options intelligently.

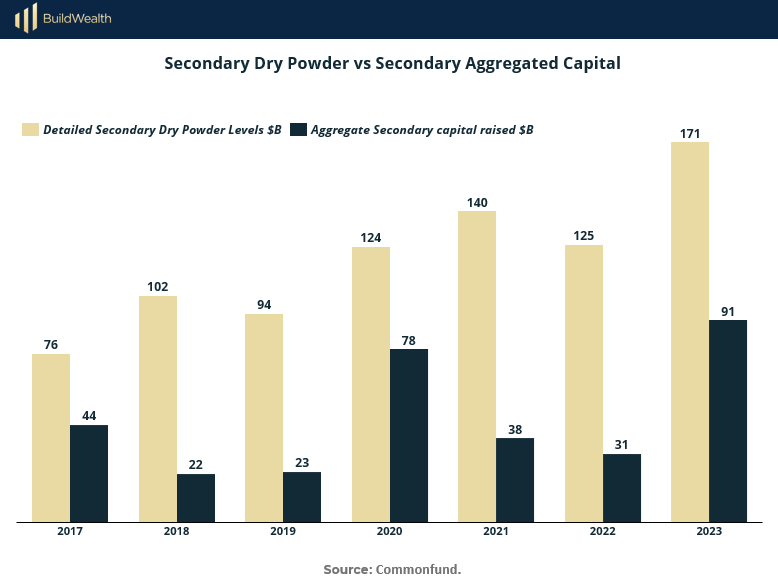

Record Dry Powder Signals Strong Future Momentum in Secondaries

While the growth of secondaries market volume tells one story, another critical piece of the puzzle is dry powder—the committed but unallocated capital waiting to be deployed. As the chart shows, dry powder in the secondaries market has surged to $171 billion in 2023, a new high.

This significant capital overhang represents not just capacity, but readiness. Funds are sitting on record levels of capital, eager to invest, which speaks volumes about institutional conviction in the opportunity set ahead.

What’s more, aggregate capital raised by secondary funds also spiked in 2023 after a brief decline. That rebound, up to $91 billion, is a powerful signal of renewed LP appetite.

As investors look for more liquidity, transparency, and control in their private market exposures, secondaries are emerging as one of the few strategies that can deliver on all three. This well-funded pipeline means the market is poised for continued innovation, larger deals, and increased participation from both buyers and sellers.

Key Takeaways for Investors:

$171B in Dry Powder = Deal Flow Confidence: That capital isn't idle—it’s primed for deployment into secondary deals, supporting future transaction volume and market depth.

2023 Rebound in Fundraising Signals Strong LP Demand: After slower fundraising in 2021–2022, capital commitments surged in 2023, showing that investors are actively allocating to secondaries again.

Dry Powder Provides Pricing Stability: With so much capital chasing deals, pricing dynamics may remain competitive, giving LPs the ability to exit positions or restructure portfolios more easily.

More Buyers, More Flexibility: Well-capitalized secondary funds can structure increasingly creative solutions—continuation vehicles, preferred equity, strip sales—to match LP needs.

A Signal of Maturity and Confidence: The dry powder buildup mirrors trends seen in other institutional asset classes, suggesting that secondaries are now viewed as a core part of the long-term private markets playbook.

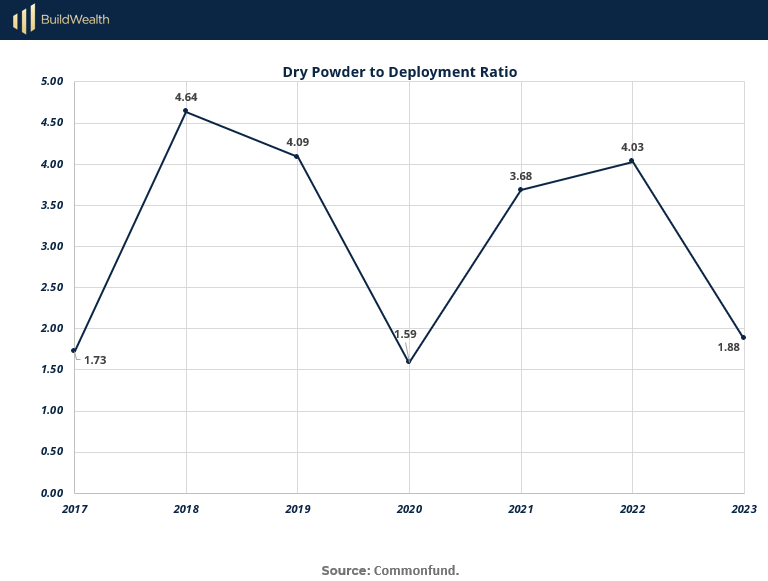

Deployment Efficiency Is Rising, And That’s Good News for Investors

While dry powder is essential for fueling future deal flow, it’s equally important to understand how efficiently that capital is being put to work. The dry powder to deployment ratio tracks just that—how many dollars are sitting idle for every dollar deployed.

A high ratio can suggest hesitation or lack of opportunity, while a lower ratio implies a more active, confident market. In 2018, this metric spiked to 4.64, meaning dry powder vastly outpaced deployment. But in 2023, the ratio dropped significantly to just 1.88—the second-lowest level in the past seven years.

This steep decline signals a turning point. With $171 billion in dry powder but a near-normalized ratio, capital is not just being raised, it’s being put to work. For allocators, that’s a strong indicator of market efficiency, fund manager confidence, and healthy deal flow.

It also suggests that many of the frictions that slowed deployment in prior years, pricing mismatches, asset uncertainty, GP hesitancy, are easing. The result is a more agile and responsive market, where capital can move with conviction.

What This Means for Investors:

2023 Ratio Drop Reflects Market Activation: A 1.88 ratio means that dry powder is being deployed much more efficiently, capital isn’t sitting idle.

Confidence in Deal Quality and Pricing: A lower ratio suggests funds are finding attractive opportunities and executing deals, not waiting on the sidelines.

Improved GP-LP Alignment: With greater deployment velocity, LPs can expect quicker drawdowns and potentially faster time-to-return dynamics on committed capital.

Sign of Market Maturity: The secondaries space is functioning with more balance—capital inflows are being matched by disciplined yet proactive capital deployment.

Now Is a Window of Opportunity: With capital still abundant and deployment active, the current market offers a favorable balance of dry powder and action—a sweet spot for investors considering entry.

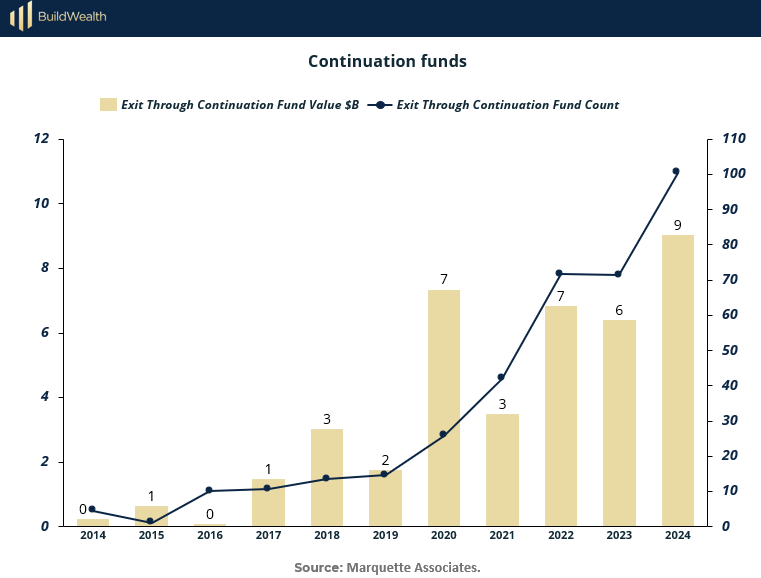

Continuation Funds: Fueling Liquidity Without Letting Go

As private equity holding periods extend and exit windows narrow, continuation funds have emerged as one of the most innovative—and increasingly mainstream—tools for liquidity. The data tells a compelling story: both the number of continuation fund transactions and their total value have grown dramatically, reaching 90 deals and $9 billion in 2024. That’s more than a 4x increase in deal value since 2018.

These vehicles allow GPs to hold on to high-performing assets by transferring them into new funds—providing liquidity for existing LPs while offering fresh upside to new investors.

This isn't just a workaround, it’s a strategic pivot. Continuation funds give sponsors more control over exit timing, valuation, and long-term exposure. For LPs, they offer optionality: sell at market price or roll into the new vehicle.

For the broader secondaries market, they’re fueling deal flow and helping private equity adapt to a world where flexibility is paramount. The recent surge in both count and value confirms that continuation funds are no longer edge-case strategies—they're now core infrastructure in modern private markets.

Strategic Insights for Investors:

$9B in 2024 Deal Value Reflects Maturity: Continuation funds are now a multi-billion-dollar sub-sector, scaling with institutional adoption and broader secondaries growth.

Volume and Velocity Are Rising: The number of continuation fund deals has reached a record 90—up sharply from under 20 just five years ago.

Tools for Portfolio Agility: These funds enable GPs to extend exposure to top-performing assets without a forced exit, while providing LPs with liquidity or rollover options.

Attractive for Both Sides of the Table: For buyers, continuation funds offer access to seasoned assets; for sellers, they unlock liquidity without market timing risk.

Embedded in the Future of Secondaries: Continuation funds are helping redefine what an “exit” looks like, shifting from binary outcomes to more tailored liquidity paths.

Conclusion: Secondaries Are the Smart Money's Next Move

The numbers tell a clear story: secondaries are no longer a Plan B, they’re becoming Plan A for a growing number of sophisticated investors. From record-breaking market volume to rising continuation fund activity and unprecedented levels of deployable capital, the secondaries ecosystem is scaling with speed, depth, and purpose.

This is about more than liquidity. It’s about building smarter, more flexible private market portfolios that can adapt across cycles. Secondaries give investors the ability to buy into seasoned assets with known performance, reduce blind-pool risk, and gain access to high-quality positions at potentially attractive valuations.

As the private equity market evolves, those who understand and leverage secondaries will be better positioned, not just to navigate volatility, but to capitalize on it. For forward-thinking allocators, this isn’t just an opportunity. It’s an edge.

Sources & references

Marquette Associates (2024). The Growing Popularity of Continuation Funds. https://www.marquetteassociates.com/wp-content/uploads/2024/05/The-Growing-Popularity-of-Continuation-Funds.pdf

Lazard (2024). Secondary Market Report 2023. https://www.lazard.com/media/4olcdlm2/lazard-2023-secondary-market-report.pdf

Commonfund.org (2024). Cash is Queen. https://www.commonfund.org/cf-private-equity/cash-is-queen-a-secondaries-article

S&P Global (2024). Private equity's annual exit total flat in 2023. https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/private-equity-s-annual-exit-total-flat-in-2023-80071407

Ey (2024). Are you harnessing the growth and resilience of private capital? https://www.ey.com/en_gl/insights/private-business/are-you-harnessing-the-growth-and-resilience-of-private-capital#:~:text=The%20rise%20and%20rise%20of%20private%20capital&text=For%20more%20than%20a%20decade,by%20the%20end%20of%202023.

JPMorgan (2024). The rising tide of secondaries: investors seek private market liquidity. https://www.jpmorgan.com/content/dam/jpm/cib/complex/content/securities-services/fund-services/rising-tide-secondaries-private-market-liquidity.pdf

Premium Perks

Since you are an Wealth Stack Subscriber, you get access to all the full length reports our research team makes every week. Interested in learning all the hard data behind the article? If so, this report is just for you.

Want to check the other reports? Visit our website.