Politicians and institutions have doubled down on ESG mandates. The narrative has been clear: oil and gas are relics of the past.

But the data tells a different story.

Global and US demand for oil and gas remains resilient — and in many sectors, it is still growing. Meanwhile, supply is quietly eroding beneath the surface. Years of chronic underinvestment, accelerating well declines, and a dramatic retreat of private equity capital are compounding to create a structural imbalance: demand is outpacing supply, and few are willing to fund the new production needed to fill the gap.

This is not a temporary misalignment. It is the result of deep structural forces that will shape energy markets — and real asset returns — for years to come. While many investors are underweight or avoiding the sector entirely, sophisticated capital is finding asymmetric opportunities: cash-flowing wells, undervalued producing assets, and advantaged positions in markets where scarcity will drive pricing power.

This report brings together the key data points that underpin this thesis:

Demand trends vs. constrained supply

Well-level decline rates driving structural supply decay

The collapse of private equity investment in upstream oil and gas

Where capital is flowing — and more importantly, where it isn’t

The message is clear: the supply side of the market is broken. For investors who understand this dynamic, the opportunity is both real and actionable.

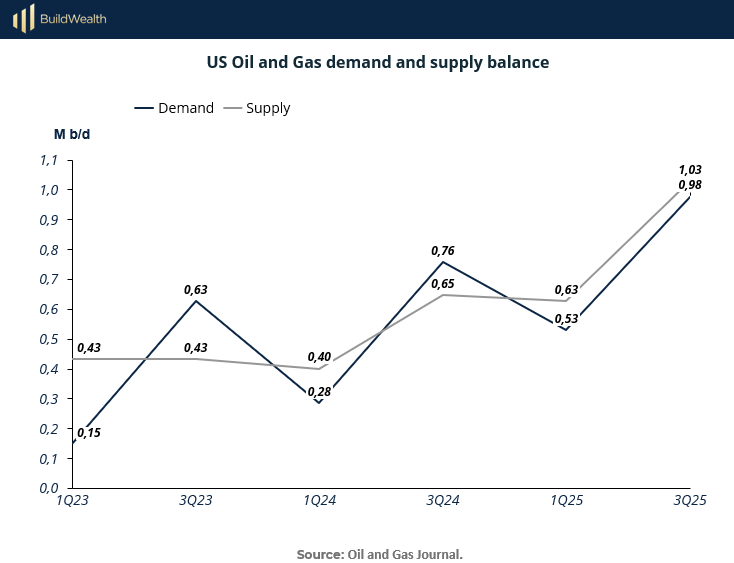

US Oil and Gas Demand and Supply Balance

One of the great investment fallacies of the past decade is that the transition to renewables would render oil and gas obsolete. But when we look at the hard data, a very different story emerges. Energy demand continues to grow in the US and globally—driven by population growth, industrial activity, and the hard reality that wind and solar cannot yet replace hydrocarbons at scale.

Meanwhile, ESG mandates, political headwinds, and chronic underinvestment have hampered new supply development. The result? A visible and widening mismatch between demand and supply.

This chart tracks quarterly US oil and gas demand versus supply, from Q1 2023 through a projection for Q3 2025. What it reveals is both simple and powerful: demand is surging, while supply is unable to keep pace.

The forces driving this imbalance are structural, not cyclical. On the demand side, transportation, petrochemicals, and industrial processes remain energy intensive and oil-dependent. On the supply side, capital constraints and declining production from existing wells are limiting output growth. For opportunistic investors, this is the signal amid the noise—a setup that can drive cash flow and price appreciation for years to come.

Key takeaways for investors:

Sharp demand growth: US oil and gas demand rises from just 0.15 M b/d in Q1 2023 to a projected 1.03 M b/d in Q3 2025—an increase of nearly 7x over the period. This trend reflects sustained end-use demand across multiple sectors.

Constrained supply response: Supply growth is far more muted, increasing from 0.43 M b/d to just 0.98 M b/d over the same timeframe. The supply curve is structurally limited by years of underinvestment and natural well decline rates.

Emerging structural imbalance: The gap between demand and supply is expected to widen meaningfully by Q3 2025, with projected demand outpacing supply. This divergence creates upward price pressure and a more favorable margin environment for producers.

Signals for investors: In an environment where many investors are underweight or outright avoiding oil & gas, this demand-supply imbalance signals a contrarian opportunity. Well-selected producing assets and development projects are positioned to deliver strong cash yields and capital gains.

Reinforcing the thesis: This chart is a microcosm of the broader global trend. US market dynamics mirror global patterns—where demand resilience meets investment scarcity, creating one of the clearest real asset opportunities in today’s market.

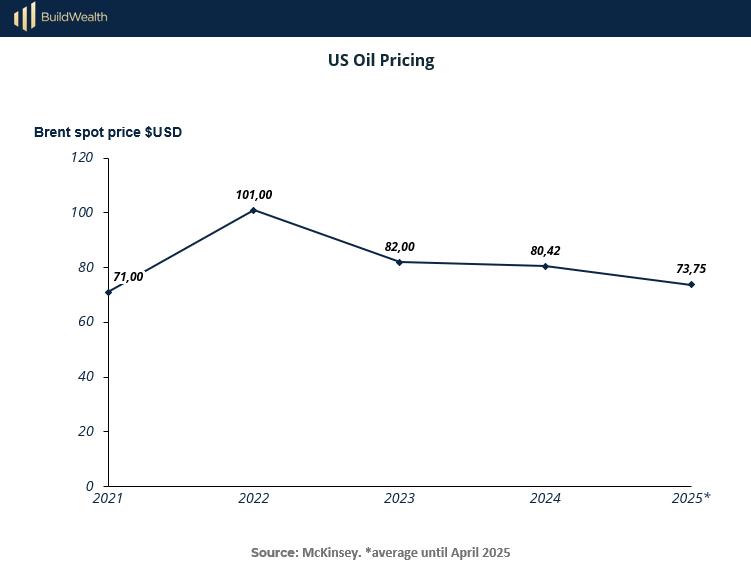

Global Oil pricing going down

Oil pricing sits at the heart of the energy investing equation. The Brent crude oil spot price—shown here—is the global benchmark for oil traded on the spot market, meaning oil purchased for immediate delivery, as opposed to futures contracts.

It serves as the primary reference price for roughly two-thirds of the world’s internationally traded crude oil, including much of what influences US pricing dynamics. For investors in oil and gas assets, the Brent spot price directly impacts revenue, profit margins, and ultimately cash flow.

This chart tracks the Brent spot price from 2021 through an average projection for 2025. The data shows clear cyclicality, but also highlights an important insight: despite geopolitical shocks, economic uncertainty, and significant investment headwinds, oil prices remain structurally elevated well above pre-pandemic levels.

A pullback from the 2022 peak is visible—but the projected stabilization in the $70–$80 range suggests a highly investable environment for cash-flow-driven oil and gas strategies. In other words, prices are settling into a new normal that continues to support strong economics for well-selected producing assets.

Key insights for investors:

Brent spot price defined: The Brent spot price is the real-time market price for Brent crude oil, the world’s leading benchmark grade. It reflects the actual traded value for immediate delivery and is a proxy for global oil pricing dynamics.

Cyclicality with higher floor: After rising from $71 in 2021 to a peak of $101 in 2022 (driven by post-pandemic demand recovery and geopolitical factors), prices have moderated but remain resilient. The projected $73.75 in 2025 reflects a much higher floor than the $40–$60 averages seen in the previous decade.

Structural price support: The persistence of prices near or above $70, despite slowing global growth and modest demand uncertainty, signals the underlying supply constraints and production discipline now governing the market.

Attractive margin environment: For Build Wealth’s strategy—focused on acquiring existing producing wells and boosting yield through infill drilling—this pricing environment supports robust margins and attractive cash-on-cash returns. Many of the wells targeted are economic even at much lower price thresholds.

Thesis reinforcement: This chart complements the prior demand-supply balance data: with demand steady and supply constrained, pricing remains fundamentally supported. For investors, this is a signal of durability—oil pricing is not collapsing under transition narratives, but stabilizing in a profitable range.

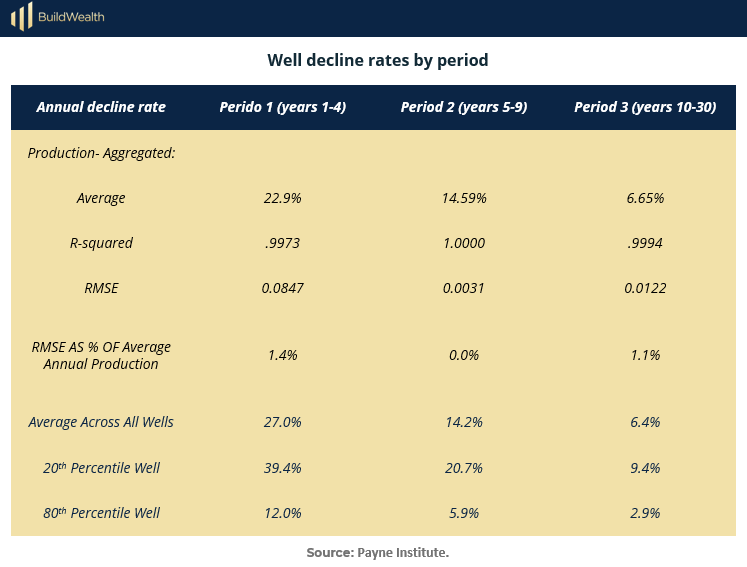

Well Decline Rates: The Mathematics of Structural Supply Decay

If investors want to understand why US oil and gas supply is structurally constrained, they must start here—with the cold, hard mathematics of well decline. Every oil and gas well follows a predictable production curve: high initial output followed by a steady reduction in flow as reservoir pressure drops and hydrocarbons are depleted. This is not a matter of operator preference or drilling technique—it is fundamental physics. Without massive reinvestment to drill new wells, total supply across a basin or market will inexorably decline.

This chart, drawn from the Payne Institute’s extensive study of over 14,000 high-quality wells, quantifies that reality across three key life stages of production. The takeaway is stark: decline is relentless, and the industry is no longer investing enough to offset it. In an environment where capital is scarce, ESG pressures are mounting, and political risks are high, this decline dynamic becomes a powerful driver of future supply gaps—and a core reason we believe existing cash-flowing assets will appreciate sharply in value.

Key Takeaways:

Terminal Decline is real and well understood: In the late-life phase (Period 3: years 10–30), wells show an average annual production decline of 6.65%, with most falling between 2.9% and 9.4% depending on percentile. This means a typical mature well loses ~6–7% of its output every year—even without operational issues or external shocks.

Compounding decline across the system: These individual well declines compound across entire basins and markets. Without constant new drilling to backfill the loss, total US supply heads downward structurally.

Early years are even more aggressive: Wells decline at a staggering 22.9% annually in years 1–4, and 14.59% in years 5–9. The moment capital inflows slow, as they have post-ESG divestment, supply erosion happens fast.

Why this matters for investors: With private equity oil & gas investment down 87.5%, US rig counts declining, and political/regulatory risks rising, the industry is not backfilling this natural decline fast enough. This creates a durable mismatch between steady demand and shrinking legacy supply.

Investment edge: Investors who understand this dynamic can capitalize by:

Acquiring producing wells with resilient flow profiles.

Valuing assets more accurately based on realistic decline expectations.

Structuring portfolios to benefit from rising commodity prices and asset scarcity.

Structural supply decay → mispriced assets: This is the core message of our thesis. As production declines mathematically year after year, and new supply fails to replace it, the value of cash-flowing oil & gas assets is poised to rise. The market is underestimating this dynamic—smart capital will not.

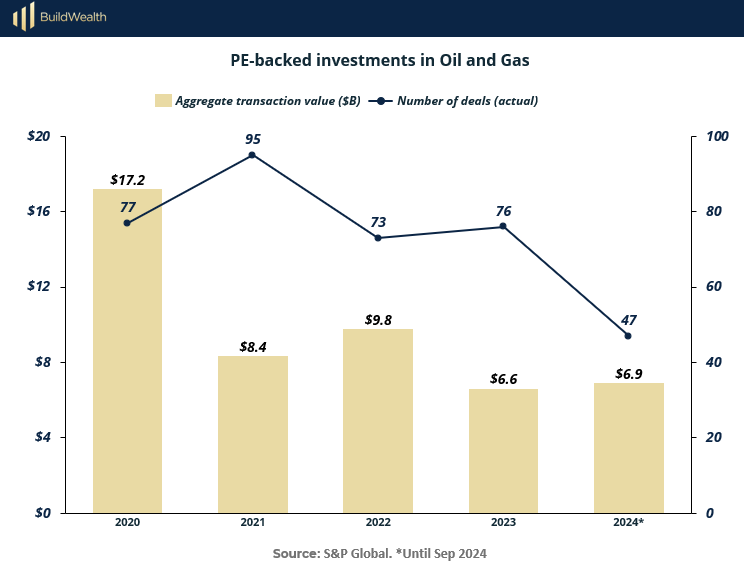

The Capital Paradox: Why Private Equity Is Missing the Oil & Gas Opportunity

One of the most striking features of today’s oil and gas market is not just that supply is structurally in decline—it’s that capital is accelerating this decline. Private equity (PE) investment, once a major force in upstream oil and gas, has steadily withdrawn from the sector.

The reasons are well documented: ESG mandates, political pressure, reputational risk, and capital reallocation toward renewables. But the paradox is this: just as supply is mathematically declining and the demand-supply imbalance is widening, many institutional investors are not stepping in—they’re stepping back.

This chart shows the trend clearly. Since 2020, both the dollar value of PE-backed deals and the number of transactions have fallen dramatically. This retreat leaves a vacuum—and an opportunity.

Fewer new wells are being drilled, existing wells are aging and declining, and high-quality producing assets are coming to market at discounts as PE funds race to meet exit timelines. Smart, flexible capital—like ours—can now acquire assets at favorable terms and generate durable yield in a market starved of supply.

Key Takeaways:

Capital is not following fundamentals: Despite a clear supply/demand imbalance, PE capital continues to exit upstream oil and gas. This creates pricing inefficiencies and leaves high-quality producing assets undervalued.

Sharp drop in investment: Aggregate PE-backed transaction value fell from $17.2B in 2020 to just $6.9B YTD 2024—a 60%+ decline. Meanwhile, the number of deals fell from 95 in 2021 to 47 in 2024, a 50%+ decline.

Why this matters: Oil and gas production is capital intensive. Without sustained reinvestment, natural well declines (as shown previously) will steadily erode total supply. The decline in PE investment ensures this erosion continues unchecked.

Forced exits create opportunity: Many PE funds are facing internal timelines forcing them to exit oil and gas positions—even if it means selling into a market with strong fundamentals. This creates a unique window for yield-focused investors to acquire assets at discounts.

The capital paradox: Most capital is acting as if oil demand is going away. The data shows otherwise—demand is stable to rising, supply is shrinking. The divergence between capital behavior and market fundamentals is precisely where outsized returns are born.

Core thesis alignment: This trend reinforces our central message: structural supply decline + capital retreat = scarcity premium ahead. We aim to position our investors to benefit from this dynamic while others remain on the sidelines.

What the Largest Deals Tell Us: Capital Is Shifting Away From Core Supply

Looking beneath the surface of the private equity activity in 2024 reveals another layer of the supply-side story. It’s not just that PE investment in oil and gas is declining in aggregate — it’s also that the nature of the deals being done reflects growing aversion to traditional upstream production. The largest PE-backed transactions this year are concentrated in infrastructure, midstream, and diversified energy services — not in the core drilling and development of new oil supply.

This chart of the largest PE-backed oil and gas deals of 2024 highlights that trend clearly. While headline transaction values may look impressive, much of the capital is flowing into low-decline assets (pipelines, LNG infrastructure), regulated utilities, and energy transition-adjacent businesses. Very little capital is going toward the type of upstream drilling required to offset structural production declines. This reinforces our core thesis: as capital avoids traditional production, the decline in supply will accelerate—and the value of existing producing assets will rise.

Key Takeaways:

Shift away from upstream: The largest 2024 deals show a clear tilt toward infrastructure (pipelines, gas utilities) and diversified or energy-transition assets—not traditional upstream drilling.

Example: Top deals include U.S. Silica Holdings, New Mexico Gas Co., and CenterPoint Energy gas utilities—none of which add new oil supply.

Even large E&P deals (e.g. Carlyle’s Italy/Egypt/Croatia portfolio) are focused outside the US.

Infrastructure is the safe play: PE capital prefers low-decline, toll-like revenue assets (midstream, LNG) over the perceived risks of new upstream production.

Supply erosion is the result: With little PE capital funding new drilling, US oil supply will continue to erode under natural decline curves—as shown in previous sections.

Opportunity in cash-flowing wells: While PE chases “safe” assets, high-quality producing wells in the US are trading at discounts as PE funds divest. This creates a unique window for well-positioned investors to acquire assets that will become more valuable as supply tightens.

Core thesis alignment: The pattern seen here reinforces the larger narrative:

Supply is in structural decline.

Capital is not funding replacement supply.

Existing cash-flowing assets will appreciate disproportionately.

Sophisticated capital that steps into this gap can capture durable yield and scarcity-driven upside.

Conclusion

The energy markets are at an inflection point. On one side of the ledger, demand for oil and gas continues to hold — supported by global economic activity, industrial demand, and an energy transition that remains incomplete. On the other side, supply is in structural decline — constrained by natural well declines, capital flight, and political headwinds.

Most institutional capital is missing this. Private equity has pulled back dramatically, both in volume and focus, leaving a vacuum in upstream investment. Meanwhile, the market for existing producing assets remains inefficient, with many high-quality wells available at attractive valuations as funds are forced to exit.

This is where smart, flexible capital can win.

By acquiring and optimizing producing wells in a capital-starved market

By focusing on real assets that generate durable cash flow and inflation protection

By stepping into a sector where scarcity is the story of the next decade

Oil and gas is not dead — it is misunderstood. And in that misunderstanding lies opportunity.

We see this as one of the most compelling private market opportunities today: a durable, yield-driven strategy in the world’s most traded commodity

The market is underestimating this dynamic.

Smart investors will not.

Sources & references

McKinsey. Oil and Gas 2025. https://www.mckinsey.com/industries/oil-and-gas/contact-us/~/media/65E578758C0642A584E053452D75CEFB.ashx

S&P Global. PE moves into fossil fuels. https://www.spglobal.com/market-intelligence/en/news-insights/articles/2024/9/private-equity-moves-into-fossil-fuels-as-genai-drives-energy-demand-83114853

OGJ. Global Oil Demand forecast. https://www.ogj.com/general-interest/economics-markets/article/55267852/iea-increases-2025-global-oil-demand-forecasts

IEA. Oil market Report April 2025. https://www.iea.org/reports/oil-market-report-april-2025

Premium Perks

Since you are an Wealth Stack Subscriber, you get access to all the full length reports our research team makes every week. Interested in learning all the hard data behind the article? If so, this report is just for you.

Want to check the other reports? Visit our website.