Hi {{first_name}},

Normally I focus on the private markets, but this past week, the crypto world had its biggest shake up yet. Several things happened that perked up my ears and deserve your attention too:

The GENIUS Act passed the Senate, giving stablecoins a path towards legal status in the U.S. financial system.

Circle’s post-IPO stock soared following the legislative news, closing at 33.8% pushing stablecoin infrastructure into Wall Street territory.

Passage of the bill also boosted stock shares of crypto exchange Coinbase by 12% while trading platform Robinhood was boosted by 4%.

Walmart, Amazon, and Shopify all announced moves toward accepting USDC—crypto’s top institutional-grade stablecoin.

These are early signals that crypto—especially stablecoins and Bitcoin—is being wired into the mainstream capital stack, not just traded on the edges.

Why should you care?

Because while most investors are still chasing headlines, ultra-high-net-worth allocators have already made their move.

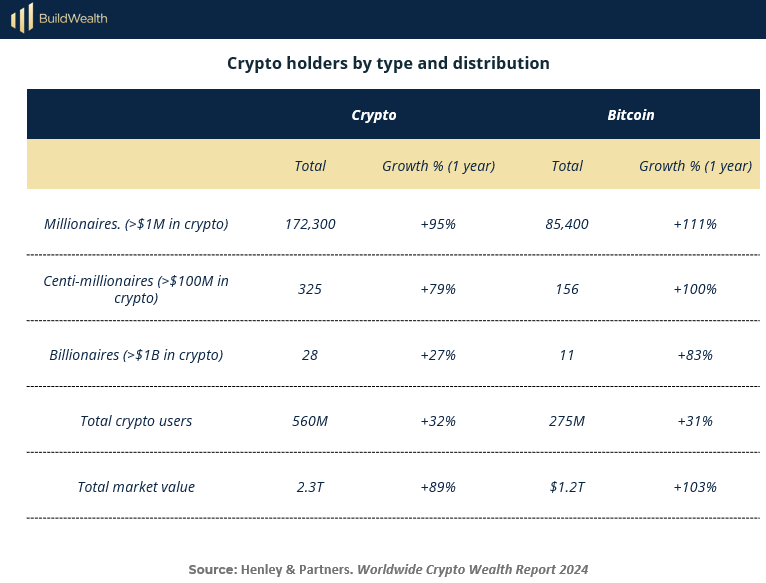

Bitcoin is showing up as a 1–5% slice in family office and endowment portfolios.

Stablecoins are being used to move capital, earn real yield, and access private credit in ways banks can’t compete with.

So if you haven’t moved in yet—consider this issue your orientation.

We’ll show you why this infrastructure shift matters. How the top LPs are positioning themselves and (importantly) what noise to ignore.

In this issue, we cover:

How MassMutual’s Bitcoin allocation signaled a new era for institutional adoption

Why tokenized private credit is delivering 14%+ yield with faster liquidity and less friction

What the GENIUS Act means for U.S. stablecoin legitimacy—and why it's a green light for LPs

A clear framework for allocating Bitcoin without trading risk

A free Excel-based Crypto Allocation Tracker to manage exposure like an institution

This is the kind of shift that changes how capital flows, not overnight, but potentially permanently. Your job is to see it early, learn how to ride the volatility, and position accordingly.

Let’s dive in.

P.S. I’m dropping something big on Wednesday the 9th. Register here to join me live: https://zoom.us/webinar/register/WN_5g1vFOThTu-fXqFmVGnH6w

SHIFT YOUR STACK

Crypto Isn’t Just an Asset. It’s Infrastructure too.

Smart investors are rethinking how capital moves, and more importantly, what it moves through.

Crypto headlines love to bring the drama — hacks, volatility, meme tokens.

But behind the noise, something real is happening:

Crypto is evolving into the financial plumbing of the private markets.

We’re talking about:

Stablecoins moving $100B+ monthly with 24/7 finality

Tokenized real assets — from credit to real estate — gaining institutional traction

Platforms like Shopify, Amazon, and Circle wiring crypto rails into mainstream finance

Congress passing the GENIUS Act, which would formally recognize digital dollars backed by Treasuries

This isn’t just a new asset class.

It’s an entirely new structure—and it's gaining adoption fast.

The Full Picture in Plain Terms

Stablecoins

Digital dollars (like USDC) that move instantly, globally, 24/7—with no banks.

Faster wires. Programmable cash. Better yield (more on this deeper down).

Tokenization

Real assets—like private credit or real estate—get turned into digital tokens that represent fractional ownership. You can buy them, sell them, earn yield from them, and track everything transparently.

Private Markets Go On-Chain

Capital allocators can now move dry powder faster, earn yield sooner, and access previously illiquid investments on modern rails.

This is what happens when the tools of crypto stop being speculative—and start being useful.

The real opportunity isn’t just in crypto.

It’s in the system crypto is building beneath your portfolio.

Smart LPs aren’t asking, “Should I own Bitcoin?”

They’re asking, “How do I own the infrastructure before the big money arrives?”

CASE STUDY

How MassMutual Quietly Stacked Bitcoin—And Signaled an Institutional Shift

The best investors don’t wait for consensus. They move quietly, early, and with conviction.

That’s exactly what MassMutual did in late 2020.

While Wall Street was still calling Bitcoin a bubble, this 174-year-old insurance company with $275B in AUM made a move no one expected:

$100 million direct allocation to Bitcoin

$5 million equity investment in NYDIG, the Bitcoin infrastructure platform

This wasn’t a headline grab or a speculative gamble. It was a strategic bet from one of the most conservative capital allocators in the country.

And it changed the conversation.

The Setup: The Fixed Income Problem

As a life insurance company, MassMutual’s mandate is clear: protect principal, deliver predictable returns, and match long-term liabilities.

But by 2020, traditional fixed income had stopped doing its job.

Treasuries were yielding close to zero. Corporate bonds were overpriced. Credit spreads were tight. And the risk-adjusted return profile looked worse every quarter.

They didn’t want more volatility. But they did need a new long-term store of value.

Enter Bitcoin.

The Stack

This wasn’t a spray-and-pray crypto play. It was a structured allocation built for institutional durability:

Core Asset – Bitcoin

A $100M direct allocation—custodied and executed through NYDIG—positioned as a long-term, asymmetric hard asset.

Infrastructure Exposure – NYDIG Equity

A $5M investment in NYDIG gave MassMutual a back-end stake in the platform facilitating institutional adoption.

Balance Sheet Discipline – 0.04% of AUM

Barely a rounding error on their books. But in institutional investing, 0.04% in a headline is a message—not a mistake.

They weren’t chasing returns. They were buying resilience.

The Outcome: Institutional Green Light

What happened next?

A wave of institutional investors took notice and have been making their own moves over the past few years:

Wisconsin pension fund disclosed in quarterly filings in early 2024 that it became the first pension to invest in Bitcoin ETFs

Harvard, Brown, and Yale have all quietly invested through third-party managers over the past few years

Abu Dhabi’s Mubadala sovereign fund has an over $400M+ Bitcoin ETF stake according to SEC filings this year

Dozens of family offices began modeling 1–3% BTC positions into core portfolios

Bitcoin didn’t just survive—it took a seat at the table.

Because when a company built on actuarial tables and death benefits says Bitcoin belongs on a balance sheet, every CIO starts paying attention.

The Takeaway: Don’t Follow the Noise—Watch the Allocators

MassMutual didn’t time the market. They observed the macro trend—and acted with size-appropriate conviction.

They weren’t being greedy. They were looking to preserve purchasing power. And they used the same logic Swensen used to build the Yale Model: when traditional tools STOP working, go BUILD new ones.

Bitcoin was their timberland. Their inflation hedge. Their non-correlated hard asset.

For LPs today, the lesson is clear:

Start small

Watch institutions

Think in decades

Because the opportunity isn’t in chasing the next token—it’s in quietly owning those that last.

BEHIND THE NUMBERS

Tokenized Private Credit: Where Stablecoins Start Earning Their Keep

How yield-hungry LPs are using stablecoin rails to tap into 12–16% private debt—with faster access and better terms

Stablecoins are gaining traction. But not just as cash alternatives.

They’re becoming capital rails—pipes for moving money into high-yield private investments at speed.

One of the most compelling early use cases?

Tokenized private credit.

Use Case: 14% Yield. 90-Day Liquidity. On-Chain.

A U.S.-based LP moves $250K in dry powder into a tokenized private lending pool. The result:

14%+ APY from short-term, asset-backed loans

Monthly payouts in USDC

Full principal liquidity in 90 days

No bank fees, no wire delays, no lockups

How it works:

Convert USD to USDC via Coinbase Prime or Circle

Allocate to a credit pool managed via smart contract

Borrowers repay interest → LPs receive instant distributions

Optional reinvestment or redemption after a lock-free window

It’s real-world lending, just faster, cheaper, and cleaner.

Why This Yield Is Real

Tokenization and stablecoin rails remove:

Manual wires

Custodial drag

Currency conversion frictions

Platform intermediaries taking basis points

Which means: More of the yield flows to the LP.

Traditional private credit has long offered high returns.

Now it has better delivery.

What LPs Are Doing

The savviest allocators we work with are using this model to:

Put idle cash to work between capital calls

Test crypto-native rails without going full DeFi

Access flexible yield without sacrificing underwriting quality

Gain asymmetric upside by being early to the platform layer

This is not about betting on the next token.

It’s about treating stablecoins like infrastructure—and using them to allocate smarter.

The Regulatory Shift Wall Street Can’t Afford to Ignore

Crypto may be volatile. But beneath the noise, stablecoins are becoming the foundation for a new layer of institutional capital movement.

They’re evolving into digitally native money-market funds:

Yielding 4–5%

Backed by Treasuries

Instantly transactable

Transparent, auditable, and global

And now the bipartisan GENIUS Act, gives stablecoins a path to legal scaffolding:

A charter

Custodial guardrails

Treasury-backed transparency

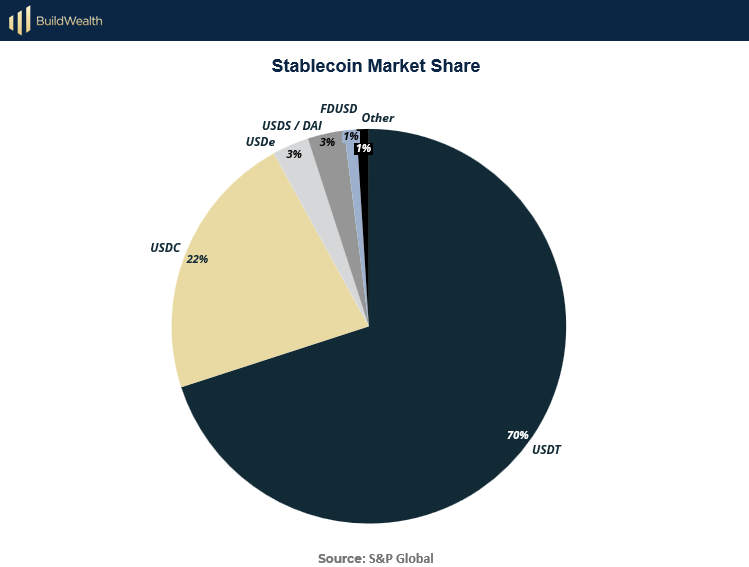

The U.S. is waking up to the reality that the digital dollar may be privately issued and that the market has already picked winners: USDC (22%) and USDT (70%) dominate in trust, liquidity, and volume.

The Real Opportunity in Crypto Isn’t Volatility — It’s Liquidity

The core value proposition of stablecoins is simple:

Low volatility, high utility, global liquidity.

But while market caps fluctuate, one thing hasn’t: yield differentials.

Right now, stablecoins offer cash-like yield with better liquidity than many fixed-income instruments.

Here’s why it's worth taking a second look:

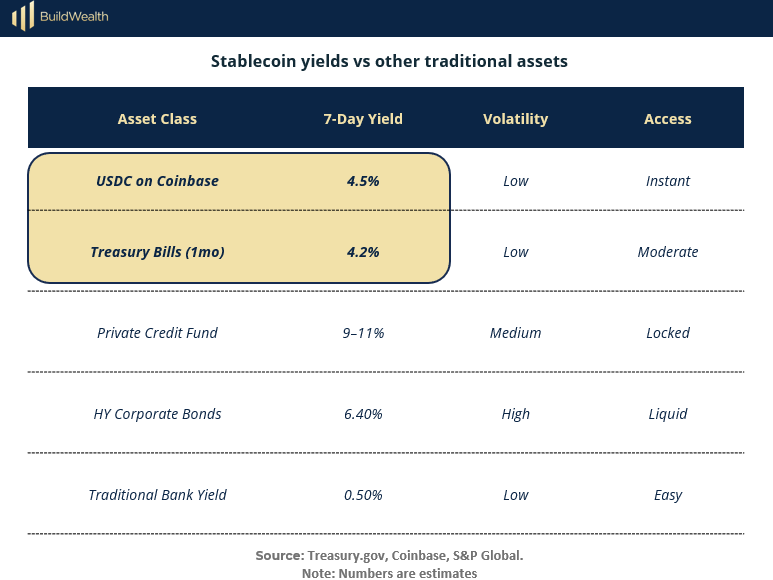

USDC on Coinbase earns approximately 4.5% — higher than 1-month T-bills.

Private credit pays more, sure. But it’s locked, typically illiquid, and higher-risk.

Stablecoins give you something else: programmable cash that pays.

Why It Matters for LPs

Stablecoins are no longer fringe—they’re a capital tool.

Not for trading. For moving, parking, and earning on cash more efficiently than traditional systems allow.

For LPs, this unlocks a more agile capital stack:

Bitcoin remains the asymmetric bet—digital hard money with long-term upside.

Stablecoins offer programmable cash with daily liquidity and real yield.

Tokenized private credit provides higher yield than traditional bonds, with faster access and institutional terms.

Regulatory clarity (via the GENIUS Act) signals that these markets are maturing—fast.

Capital allocators are using these tools to optimize idle reserves, access new deal structures, and stay one step ahead of institutional adoption.

The infrastructure is live. The use cases are working.

And the smartest LPs aren’t waiting for consensus—they’re already compounding in the background.

The market has already decided to move ahead. Stablecoins like USDT and USDC dominate with over $130B in market cap and trillions in annual on-chain volume. Regulation is still catching up, but adoption is well underway.

THE PLAYBOOK

So What Are The Richest Investors Doing? They’re Navigating Crypto’s New Infrastructure.

Statistically, UHNW investors are already positioning smart, modest allocations in crypto infrastructure.

39% of single-family offices are already investing in or exploring crypto, with average allocations close to 1.8%.

83% of institutional investors are planning to increase digital asset exposure, with 84% targeting stablecoins and tokenized assets in 2025.

This illustrates where capital is quietly repositioning and why it’s worth paying attention. Reallocating capital doesn’t just present market shifts, it helps create them.

This playbook illustrates what these UHNW allocators are doing.

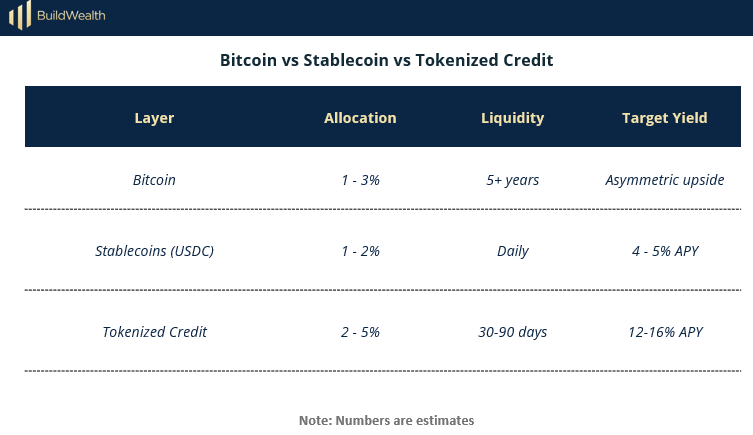

1. Anchor Allocation in the 1–5% Range

UHNW allocators are splitting this strategically:

1–3% Bitcoin: for long-term asymmetric exposure

1–2% Stablecoins (e.g. USDC): high-liquidity cash alternative with yield

2–5% Tokenized Private Credit & RWAs: high-return yield layer

That puts digital assets between 5%–8% of the total portfolio, consistent with institutional benchmarks.

2. Stack Move of the Week: Tokenize Your Dry Powder

Think of this as your digital emergency fund:

Buy and hold 1–2% in USDC via Coinbase Prime, Fireblocks, or Circle Mint

Allocate a small amount of capital into tokenized yield-bearing credit or real-world asset platforms

And—no, don’t just buy Circle stock because it’s hot. The move is to use their infrastructure, not their equity.

3. Time Your Allocations Appropriately

Each layer has a different timeline and utility:

Family offices increasingly use private credit and infrastructure to offset volatility—aligning with these tiered timelines.

4. Pick Your Wrappers Wisely

UHNW allocators prioritize:

Simplicity & compliance: Bitcoin via ETFs or Coinbase Prime

Liquidity & yield: USDC on institutional-grade platforms

Yield plus control: Permissioned tokenized credit pools with transparent structures

This is infrastructure investing not token speculation and it’s how the smart money plays it.

5. Track, Rebalance, Repeat

Apply institutional discipline:

Monitor with the Crypto Allocation Tracker and watch your drift

Rebalance quarterly along liquidity and target yield lines

Let earnings compound or redeploy based on performance and goals

Bottom Line

This is the risk-conscious digital layer top allocators are quietly stacking into their portfolios. Think of it as one-part asymmetric growth (Bitcoin), one-part efficient cash (stablecoins), and one-part yield (tokenized credit).

This approach blends opportunity with downside protection. Letting you invest in core infrastructure without getting caught up in the headlines.

WEALTH STACK TOOLBOX

Crypto Allocation Tracker for Entrepreneurial LPs

If you're dabbling in crypto, or building a serious asymmetric sleeve, you need more than vibes and price predictions. You need visibility.

This week’s spotlight is a free Excel-based Crypto Allocation Tracker. It’s a clean, flexible tool that lets you track, rebalance, and sanity-check your exposure.

No logins. No dashboards. Just cold, hard numbers in Excel—where they belong.

Why It’s Useful:

Crypto is inherently volatile. That’s the trade. But you can still treat it like a real asset class—especially if you’re allocating from a personal LP portfolio. Whether it’s 1% of your stack or 10%, the key is knowing what you own, how it’s performing, and when it’s drifting.

This tool makes that easy.

Key Features You Can Customize:

P/L and cost basis tracking by asset

Target allocation vs. actual — spot drift and rebalance

Manual transaction log to keep custody and DCA behavior clear

Fully editable — add ETF exposure, cold wallet entries, stablecoin yield sleeves

Bottom Line:

You don’t need to predict where crypto’s going.

You just need a system to track how it fits in your stack.

This tracker gives you institutional-style visibility without the institutional bloat.

Clean, simple, and built for operators who want signal, not noise.

MINDSET SHIFT

The smartest capital isn’t debating whether crypto belongs.

It’s already stacking exposure—Bitcoin for asymmetric upside, stablecoins for liquidity and yield, and tokenized credit for flexible income.

This is where capital is starting to flow—quietly, deliberately, and with a long-term lens.

You don’t have to go all in, but if you want to stay ahead of the curve, now’s the time to get positioned.

WHAT WE ARE READING

"Bitcoin is a hedge against the irresponsibility of central banks."

Paul Tudor Jones