Hi,

If you’re like me and own shares of $TSLA, this entire year has been a bit of whiplash.

Last week, Tesla stock dropped more than 14% in its worst single-day market cap loss in history. What’s remarkable about this isn’t Musk or Trump, it’s this: the decline helped drag down both the S&P 500 and Nasdaq on Thursday. Even if you don’t hold Tesla, you’re not safe from its effects.

Volatility is the silent killer of wealth. Way more than people realize.

Most investors don’t realize how destructive it really is. You can have a few good years of gains, and then one bad quarter takes you right back to zero. Not because you did anything wrong. Just because you were exposed to too much noise.

Public markets don’t care about compounding. They care about motion. Movement. Headlines. Volatility isn’t an accident—it’s built into the system.

And right now? That system is twitchy.

Yes, the S&P’s trading near all-time highs again. But don’t let that headline fool you. Under the surface:

• The Fed still sets the tone—every policy update rattles the tape.

• Core inflation remains stubbornly above 2%, and trade friction is still feeding the fire.

• And despite new highs, only a handful of mega-caps are doing the heavy lifting. That’s not strength. That’s tension.

This is where most investors get burned.

Meanwhile, the people I watch closely—the ones building actual wealth—aren’t buying the dips on ETFs and praying for rate cuts. They’re moving capital into places where volatility doesn’t show up.

Private credit. Operating businesses. Income-producing assets with real cash flow.

No daily price swings. No panic-selling. Just steady compounding growth, without the noise.

Every dollar we move at Build Wealth is a vote against volatility and for resilience. We’re not trying to beat the market. We’re opting out of the noise and playing a better game.

Inside this week’s issue:

• Why volatility is the stealth tax on your portfolio (and how the top 1% avoid it)

• How Yale built a $40B endowment by saying no to liquidity

• The 70/30 Stack: our framework for private market reallocation

• A downloadable Stack Mix Calculator to rebalance like a family office

You don’t need a Bloomberg terminal or a $100M family office to make this shift.

You just need a better plan.

Let’s build it.

SHIFT YOUR STACK

Volatility is the silent killer of wealth. Way more than people realize.

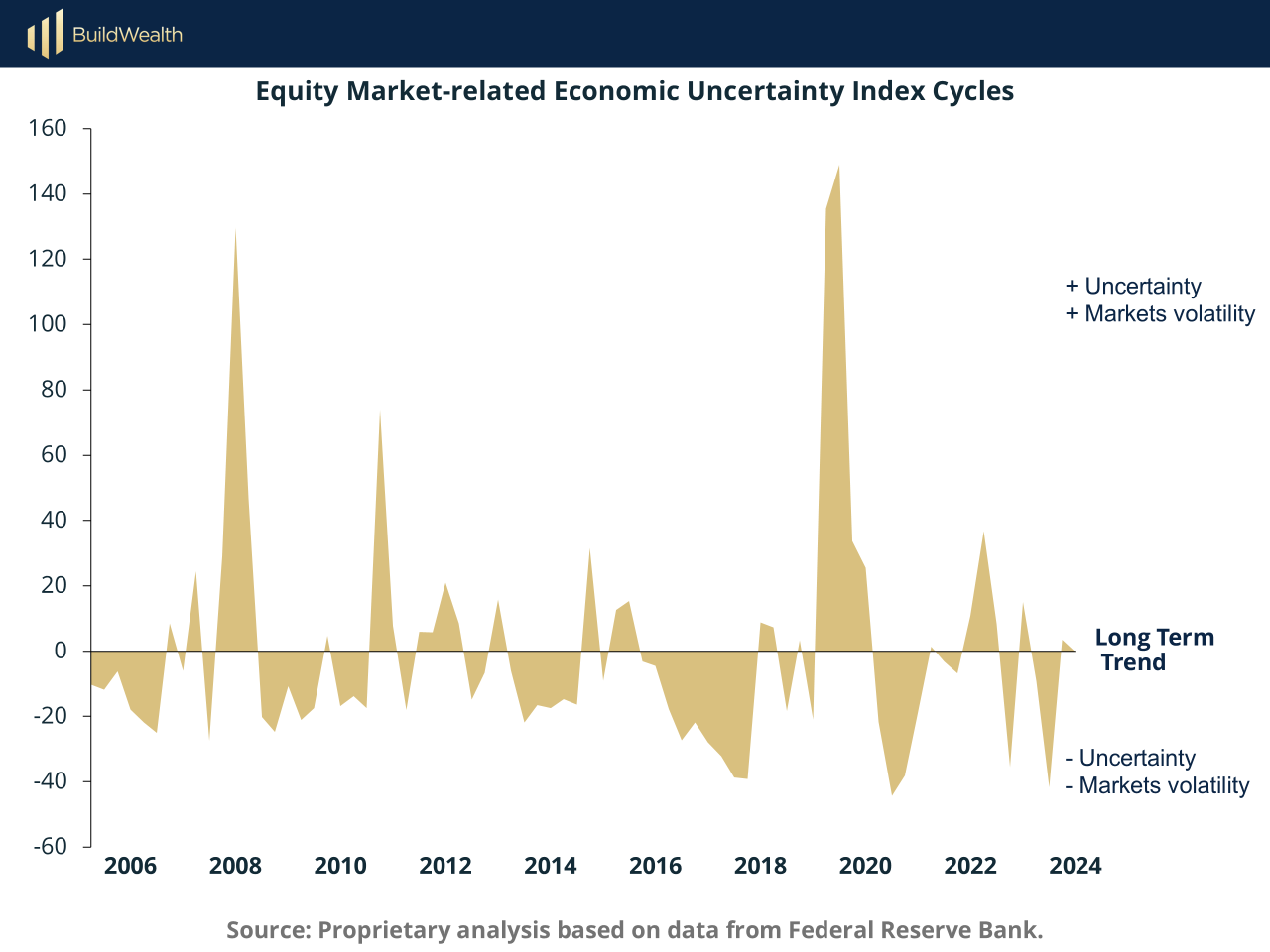

On Liberation Day in April, the VIX spiked to 57.52 its highest level since the COVID-19 pandemic. The VIX, or volatility index, measures 30 day options trades against the S&P 500.

Known as the “fear gauge”, a high VIX can indicate a coming tidal wave of uncertainty that will upend your classic 60/40 portfolio. It’s a key signal designed to distill a lot of market noise.

That noise isn’t just annoying. It’s expensive.

If you're still investing like it's 1985—dollar-cost averaging into ETFs, tracking your 401(k), hoping the “diversified” approach works—you’re playing a game that looks smart on paper… but quietly bleeds you in practice.

Since 2020, we’ve been in nonstop turbulence. GDP swings. Fed hikes at record speed. Inflation that just won’t die. Bonds and stocks moving like tech startups. It’s not a crash, but it’s constant friction—and it wears on you.

We’re all human after all. And the more optionality you have, the more likely you are to screw it up.

Because when the shocks do hit—COVID, the 2015 China crash, 2008—public capital flees based only on headlines.

This is the topic of this week’s research report, Volatility Destroys Wealth. In it, we show how $30–35 billion left emerging markets in a matter of weeks after each major panic. Not because the assets changed—but because liquidity let people react.

In contrast, we show how the private markets don't react. They absorb.

No daily pricing. No sell button. No panic loop.

And that’s the point. The wealthy don’t avoid volatility by being smarter traders. They do it by buying assets that ignore the noise entirely.

Volatility doesn’t just destroy portfolios—it destroys focus, conviction, and time. That’s the real cost.

Here’s what the ultra-wealthy figured out a long time ago:

Volatility is a tax you pay for liquidity.

CASE STUDY

How Yale Built a $40B Portfolio by Going Private

Ok, so volatility doesn’t just make your portfolio uncomfortable—it makes it inefficient.

It chips away at compounding, erodes returns, and allows for emotional decisions (at exactly the wrong time).

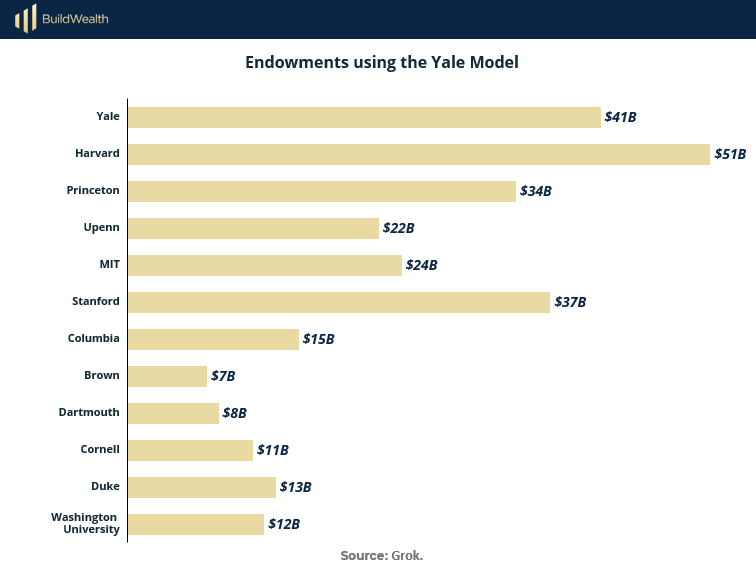

David Swensen knew this before most of us were even investing.

When he took over Yale’s endowment in 1985, it was a pretty traditional portfolio—mostly U.S. equities and bonds. By the time he passed in 2021, Yale had grown its endowment to over $40 billion—and the allocation strategy had become one of the most copied models in institutional investing.

Swensen’s core belief?

Generational wealth isn’t built in the public markets.

Most investors think liquidity equals safety. Swensen flipped that completely. He saw liquidity for what it really is: a trade-off.

More liquidity = more volatility. More noise. Less control. Lower returns.

So he leaned into the illiquid. That’s where the inefficiencies live. That’s where alpha hides.

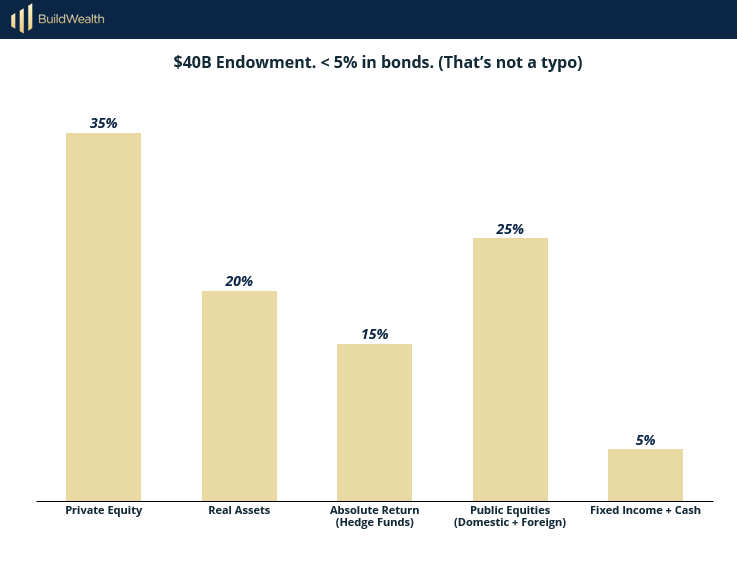

Here’s Yale’s current target allocation:

That’s 75% outside the public markets.

Swensen wasn’t chasing access–he was engineering asymmetry.

Private equity gave him long-term upside and active governance. Real assets like timber, energy, and real estate offered inflation protection and yield. Absolute return strategies added a hedge against volatility.

Public equities? Just a sliver. Not the engine—just the garnish.

This wasn’t about complexity for its own sake. It was about building a compounding machine that didn’t flinch when the headlines hit.

And it worked.

BEHIND THE NUMBERS

How the Top 0.1% Allocate Their Wealth

Most investors are flying blind when it comes to portfolio construction. They follow outdated rules of thumb (“60/40,” anyone?) or just track what their 401(k) gives them by default.

But the ultra-wealthy don’t guess. They engineer portfolios with purpose—tilting toward control, cash flow, and compounding. Let’s take a look under the hood.

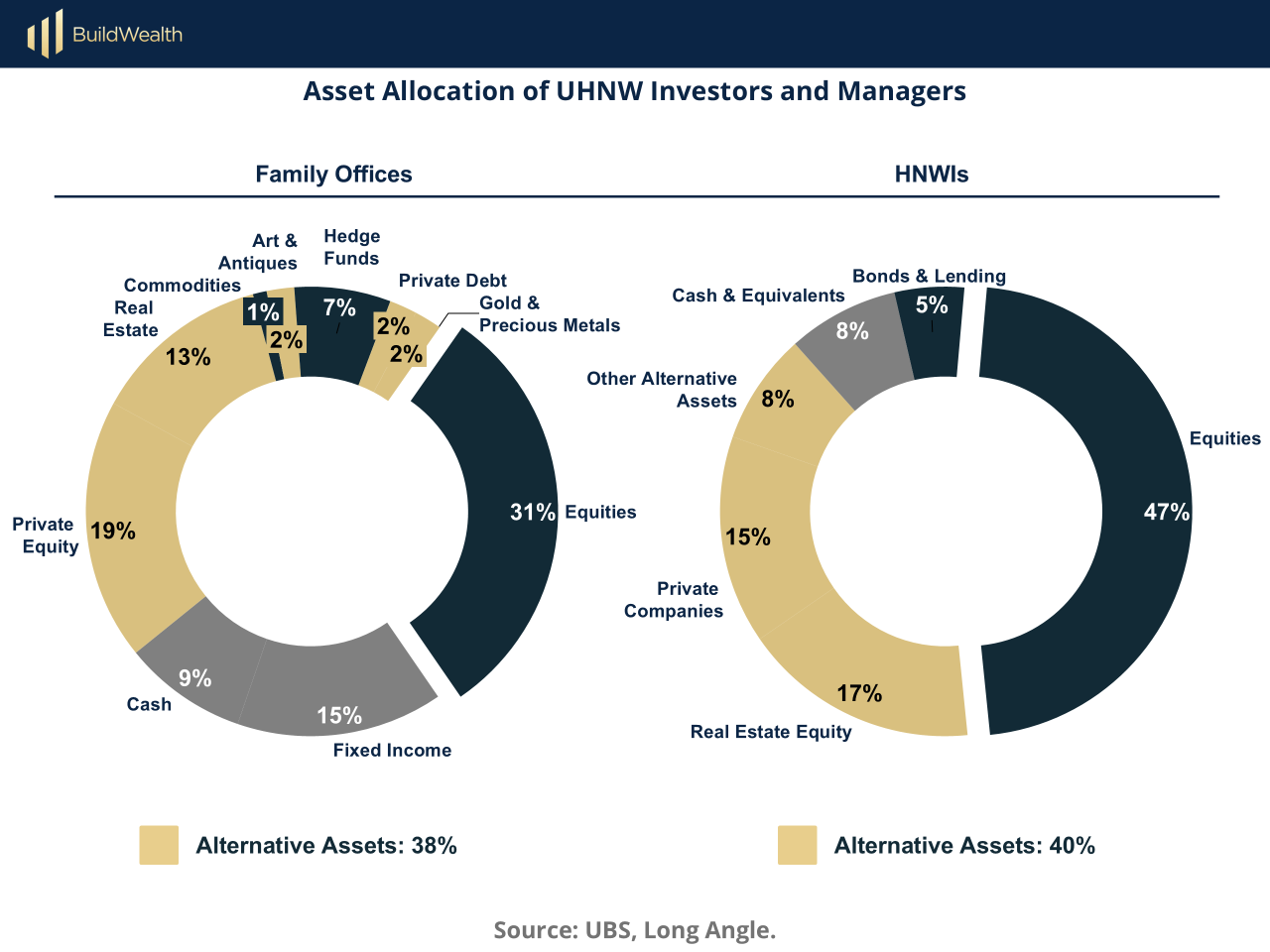

The Private Market Tilt

Here’s how UHNWI (ultra-high-net-worth individuals) and family offices typically allocate:

Sources: UBS Global Family Office Report, Tiger 21 Quarterly Allocation Report, Capgemini World Wealth Report, and BlackRock Family Office Insights.

They aren’t trying to beat the market. They’re building a different one entirely.

What You Won’t See:

Overweight tech ETFs

Liquidity obsession

Single-asset exposure

Instead, the wealthy prioritize:

Income + ownership over just appreciation

Asymmetry (controlled downside, unlimited upside)

Time horizon alignment (private assets matched to long holds)

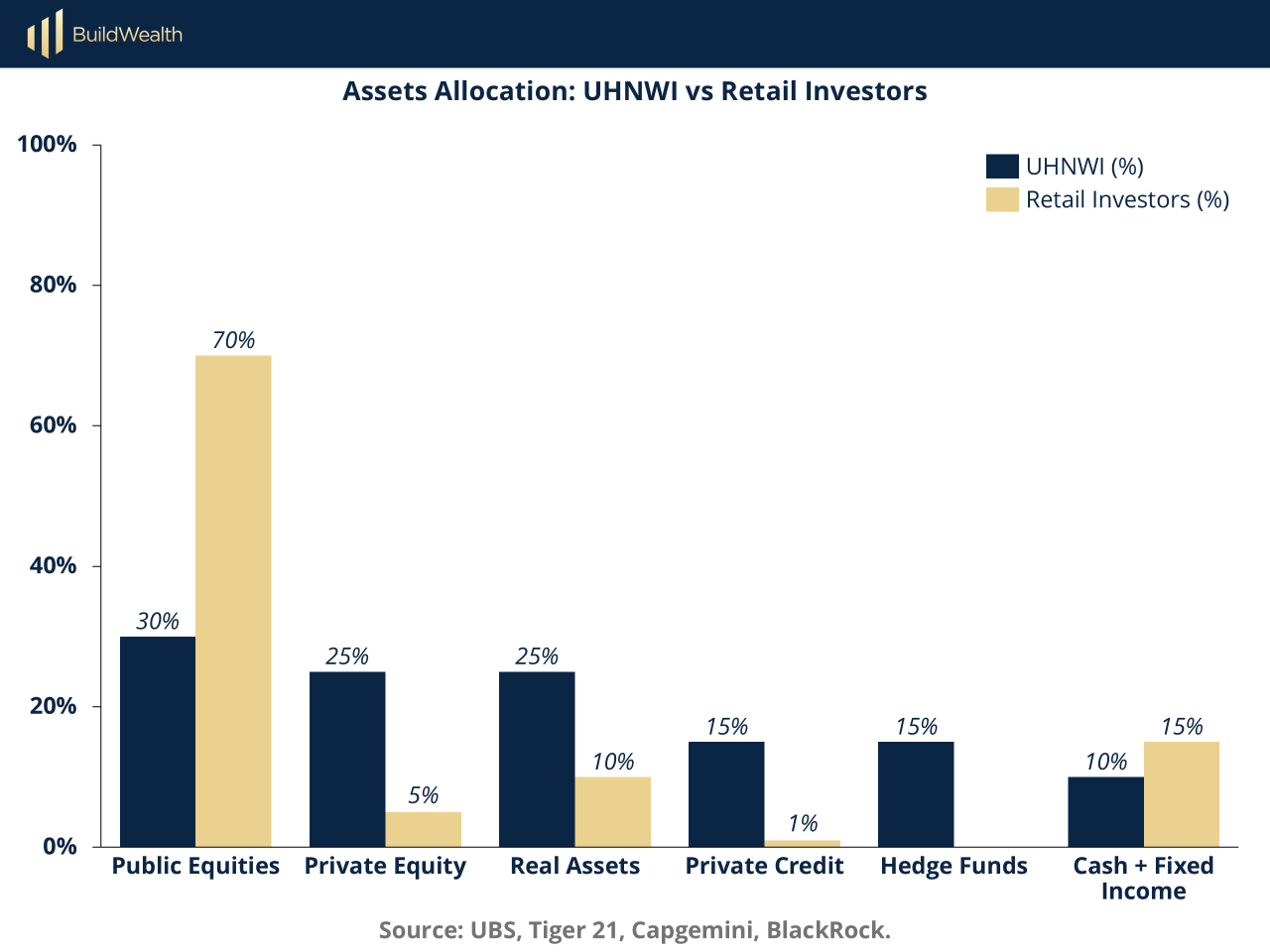

Now you understand the gap between the average millionaire and the average Ultra High Net Worth Individual.

Here it is in graph form:

Why It Works

This isn’t diversification across a single asset class (like public stocks)—it’s reconstruction. A way to hold non-correlated asset classes that together, greatly reduce volatility.

They don’t sprinkle in a few alts for flavor. They invert the pyramid. Public markets become the garnish, not the entrée.

It’s not just Yale. It’s Tiger 21, Blackstone insiders, multi-family office CIOs… They’re all building from the same blueprint—because it works.

THE PLAYBOOK

The Playbook: The Volatility Escape Plan

Rebalancing Toward a 70/30 Stack

Most portfolios are built backwards: way too much exposure to public markets, and almost no real control.

But the wealthiest investors don’t just diversify—they reallocate away from chaos. They structure their portfolios to avoid volatility altogether.

Here’s how to start doing the same:

Step 1: Define Your Investable Net Worth

Not everything you own is investable. Strip out your home equity, emergency fund, and anything you’re not willing to risk. What’s left? That’s your investable capital.

That number is your foundation. Everything else is noise.

Step 2: Time-Lock Your Capital

Money doesn’t just have a job—it has a timeline. Break your capital into buckets:

1–3 Years: Liquidity needs (reserves, cash equivalents)

3–7 Years: Mid-horizon plays (private credit, income real estate)

7+ Years: Long-term builders (operating businesses, PE holds, venture)

Volatility only hurts when it intersects with liquidity. Time-align your risk.

Step 3: Audit Your Current Exposure

Most investors are 80–90% public equities—not by design, but by default.

Chart your current mix:

Public equities

Private investments (real estate, credit, businesses)

Cash and bonds

Alternatives

You can’t shift course if you don’t know where you’re starting.

Step 4: Model Your Future Stack

Use our [Stack Mix Calculator] to simulate new allocations. Start with the Wealth Stack baseline:

30% Public

70% Private

Inside that 70%:

40% Real Assets (income real estate, farmland, infrastructure)

20% Private Credit (secured lending, debt funds)

10% Operating Businesses (direct ownership or fractional)

Tweak it based on your income, taxes, and risk profile.

Step 5: Reallocate with Intention

You don’t have to do it all at once. Redirect savings, distributions, and bonuses toward your new stack. Shift steadily. Reinvest wisely.

This isn’t trading. It’s construction.

Each dollar you move into the private side is a dollar less exposed to panic—and better positioned for asymmetric upside.

Think Like a Builder

Volatility destroys compounding. Private markets restore control.

This isn’t about abandoning public markets altogether. It’s about giving them the role they were meant to play: liquid, accessible—but not dominant.

Your real wealth? That lives in the 70%.

Where you own the asset. Control the upside. And stop waking up to headline induced panic.This is the foundation for lasting wealth. Let’s build it right.

Want help building your 70/30 Stack?

Download the [Stack Mix Calculator] or book a strategy call with our team.

WEALTH STACK TOOLBOX

Stack Mix Allocation Calculator

This one-page tool helps you audit how your wealth is actually allocated—so you can start investing like an LP, not a retail trader.

You’ll drop in your current holdings across seven core asset classes, then benchmark your public/private exposure against elite models like Tiger 21 and the Yale Endowment. Run your own scenarios and see how shifting just 10–20% can dramatically improve diversification, liquidity alignment, and long-term compounding.

Use It To:

Audit your current allocation with institutional clarity

Compare your mix to ultra-wealthy investors and endowments

Run private vs. public allocation scenarios

Identify where your current mix may be working against you

Customize the tool to your own holdings and preferences to get a picture of your Stack Mix.

WHAT WE ARE READING

THE ONE SHIFT THAT CHANGES EVERYTHING

Stack Mix Allocation Calculator

Most investors spend years chasing higher returns—when the real win is simply protecting what you’ve already earned.

Volatility doesn’t just create stress. It steals time.

It forces decisions. Distracts you from the plan.

And worst of all? It compounds in reverse.

That’s why we don’t try to outsmart the chaos anymore.

We opt out.

We use 70/30 not as a rule, but as a lens:

Earn your upside through ownership

Defend your downside with structure

Let private markets do what public ones can’t—compound without interruption

If you remember one thing from this issue, it’s this:

You don’t have to chase more. You just have to lose less.

That’s how real wealth gets built.

Let’s build yours.

P.S. What to see where I’m putting my own money to limit volatility? It’s our Private Credit Fund, BuildFlow I. It’s full for this quarter but we do have a waitlist for July. I consider this the ultimate volatility killer.

"Price is what you pay. Value is what you get"

Warren Buffet