Hi {{first_name}},

I’ve built my career acquiring what’s already working—and building from there.

That same strategy is driving one of the biggest performance shifts in private markets right now.

Secondaries.

For years, secondaries were the quiet corner of private equity. Useful. Efficient. But rarely the star.

Now? They’re outperforming.

According to Preqin and BlackRock, secondaries have consistently delivered higher median internal rate of returns (IRRs) than both buyout and growth equity strategies.

Over the last five years some have posted average IRRs north of 30%.

Why? Because secondaries change the math.

You’re stepping into known assets with real data, shorter hold periods, and often a discounted entry. You’re skipping the unknown risk, collapsing the J-curve, and getting repaid faster. While other investors are running a marathon, you’re grabbing a baton for the last mile of a relay race.

In 2024, secondaries hit $160 billion in transaction volume, with a reported $171 billion in institutional dry powder waiting to deploy. It’s a fundamental restructuring of approach.

The best investors aren’t always chasing early—they’re engineering ways to enter late.

In this week’s issue, we dig into:

Why secondaries are earning top-tier returns—and growing fast

What gaming’s rise reveals about capital allocation and exit friction

How deal structure— not just strategy—can 2x your equity returns

I’m also sharing a recent secondary offering I was able to secure for our Build Wealth investors, and how it may be opening up again…

Let’s build,

WSJ & USA Today Bestselling Author of Buy Then Build & Founder, Build Wealth

Want alternative investing insights right in your inbox? Subscribe here!

DATA DIVE

The Quiet Corner of Private Markets Just Got Loud

There’s a part of private equity most investors have never touched. It's quieter than growth equity. Less flashy than venture. And yet—it’s becoming one of the smartest places to deploy capital in 2025.

We’re talking about secondaries—and they’re surging.

In 2024, the secondary market achieved a record-breaking transaction volume of $160 billion, surpassing the previous high set in 2021. This surge reflects the market’s exceptional ability to innovate and adapt, attracting a broader range of participants and delivering tailored solutions to meet the growing demands for liquidity and portfolio management.

So what are they?

Secondaries involve the buying and selling of existing positions in private equity funds or privately held companies. Instead of betting early and waiting years for an exit, secondary buyers step in midstream—often acquiring high-quality assets at a discount.

That’s a big shift. And here’s why it matters now:

Faster, more predictable returns. You’re not betting on potential—you’re buying into real assets with performance history.

A liquidity engine in a slow-exit world. With IPOs and M&A activity still lagging, secondaries let investors recycle capital and sponsors reshape portfolios—without waiting on the public markets.

Capital efficiency on a new level. The secondary market's growth has been accompanied by a greater use of leverage by secondaries funds, enhancing capital efficiency.

The takeaway?

In this week’s Data Dive, we unpack:

Why secondaries are entering their breakout moment

How continuation vehicles are reshaping liquidity and control

What this flood of transaction volume signals for pricing, access, and alpha

If you’ve never looked at this corner of the private markets—now’s the time.

Read the Full Guide: Secondaries, the Quiet Giant that Just Got Loud (more)

BEHIND THE NUMBERS

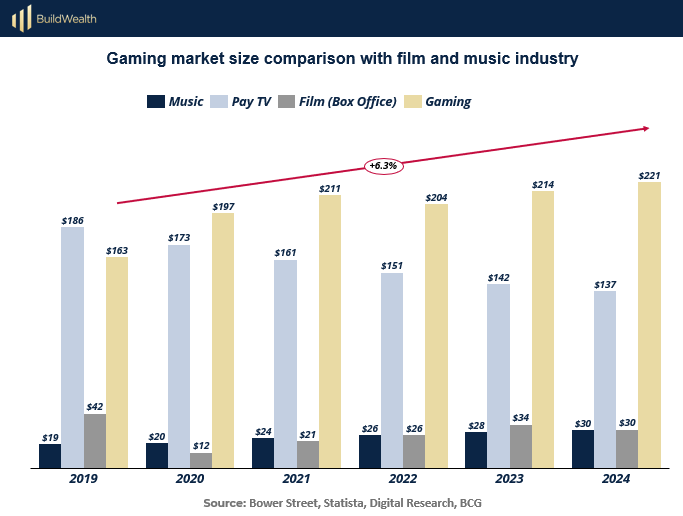

Gaming is Like, Really, Really Large… and Growing

Most people still think of “gaming” (as in video games) as a consumer trend. But sophisticated investors know better: this is one of the largest, most durable media ecosystems on the planet.

In 2024, the global gaming industry generated approximately $187.7 billion in revenue, surpassing the combined revenues of the global film and music industries.

Said another way, Gaming is bigger than Hollywood, television, and music—combined. And it’s growing faster.

If you’re allocating capital and not paying attention to that scale, you’re missing the signal. And just like film and music before it, gaming’s unprecedented growth is creating ripple effects across the capital stack: in how deals are structured, how liquidity is engineered, and how long investors hold.

When a Market Gets This Big, It Behaves Differently

As industries mature, a pattern emerges:

Traditional exits (IPOs, M&A) slow down

Ownership timelines stretch

Liquidity pressure builds

And capital gets more creative

Sound familiar? It’s the same structural shift we’re seeing across private equity—and why the secondaries market is booming.

This same trend is visible in gaming. Whether it’s a AAA studio recapitalizing via private equity or a GP rolling prized IP into a continuation fund, the logic is the same:

Massive markets demand flexible exits. And a liquidity need for one, is a buying opportunity for another.

The New Play

Want exposure to gaming? You’re not limited to early-stage startups or public behemoths. The real opportunity is in late-stage private vehicles and secondaries—where IP is mature, users are sticky, and cash flow is real.

We may expand our Delphi Interactive Inc. offering as early as this week—the studio behind the upcoming 007 game (yes, James Bond!). Full write up in The Hidden Gem section below.

This deal was only available via Build Wealth, and if extended, will NOT be available anywhere else. It’s a way I can offer secondaries in a capital-intensive sector where few retail LPs get access.

If you want to learn more, you can review the deal and connect with us here.

At the same time:

If you’re holding long-duration assets anywhere in the private markets—adding secondary sales to your playbook can prove to be very profitable.

Follow the Capital

Want to understand where the next outsized gains will come from? Track where institutional capital is going.

Right now, it’s flowing into:

High-retention sectors like gaming

High-efficiency strategies like secondaries

Flexible structures that offer liquidity without a full exit

The Big Picture

When an industry outgrows its infrastructure, new markets emerge to support it. That’s what happened when film gave rise to streaming. That’s what’s happening in gaming right now.

And that’s exactly what secondaries are doing across the entire private market landscape.

The next trillion-dollar opportunity will come from reinventing how we own the ones we already have.

THE PLAYBOOK

The LP Playbook: How to Evaluate (and Win in) Secondaries

Secondaries are still complex and relationship-driven, sure; but they also require a shift in thinking.

Here’s your step-by-step guide to spotting a good secondary deal—and understanding the terrain before you invest your cash.

Step 1: Know What You're Buying

There are three main flavors of secondaries:

LP Secondaries – You’re buying someone else’s stake in a fund that’s already years into its lifecycle.

GP-Led Secondaries (Continuation Funds) – The sponsor keeps a strong asset and rolls it into a new vehicle, letting early investors exit and new ones enter.

Direct Secondaries – You buy private shares in a company from an early employee, founder, or previous investor.

Each offers different timelines, return profiles, and risk exposures. The key is knowing which fits your objectives and cash flow needs.

Step 2: Look for Real Asset Visibility

Good secondaries aren’t a blind bet. You’re stepping into a live company with an actual track record—not just optimism and pitch decks. Remember Buy Then Build? Make sure you’re buying a real company (or into a fund of real companies).

How much data can I see on the underlying company?

What is the current valuation based on?

Are these assets already cash-flowing or near-exit?

What are the projections moving forward? How has the team performed prior projections?

If a fund: What percentage of the fund’s net asset value (NAV) is in exited vs. active investments?

Step 3: Understand the Waterfall

Most LPs get buried under waterfalls with the best “alignment” intentions, or because an institutional investor had negotiated a cheat code to get in front of everyone else.

Get crystal clear on:

Preferred return thresholds

Any outstanding convertible debt

Catch-up mechanics

Equity splits after the pref

Bad terms in a good deal = subpar, or non-existent, returns.

Great terms in an average deal = serious wealth-building.

Getting your money back, and potentially to the upside faster, is the goal of many secondary investments.

Step 4: Discount Drives Alpha (But Context Matters)

Secondaries often come at a discount to enterprise value (or NAV if a fund). But not all discounts are equal.

Is the discount due to timing (e.g., end-of-fund-life), or distress?

How recent and reliable is the valuation?

Does the discount compensate for illiquidity, or signal deeper issues?

Don’t get hung up on a discount amount: Sometimes a 0% discount on a pristine asset beats a 25% discount on something sketchy.

Step 4: Evaluate GP and Seller Incentives

Whether it’s LP-led or GP-led, alignment matters.

In GP-led deals: Is the sponsor reinvesting alongside new LPs?

In continuation funds: Why isn’t the sponsor selling? What’s the growth thesis?

In LP trades: Is this a strategic rebalance, or a distressed exit?

A good secondary deal is built on mutual benefit—not just someone else offloading risk.

Step 5: Watch the Duration and Liquidity Profile

One of the biggest benefits of secondaries is a shorter hold period. Many secondaries target liquidity in 3–5 years instead of 7–10.

What’s the expected duration of this investment?

Are distributions expected soon, or is it a long reinvestment runway?

Does this help balance my portfolio's J-curve exposure?

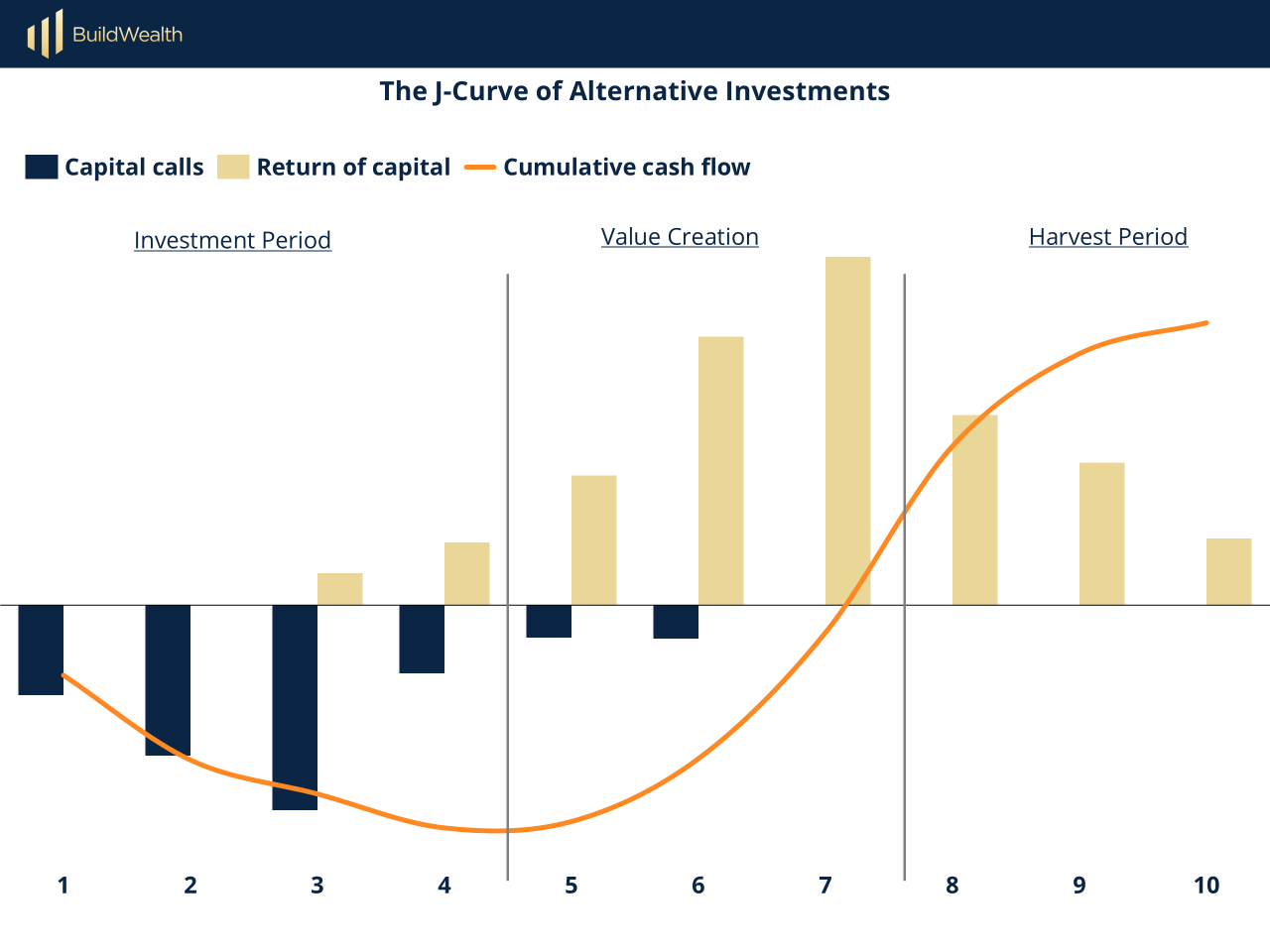

The Secondary Return Curve: Why Mid-Cycle Outperforms

Here’s what returns actually look like in private deals:

Early years = reinvestment, infrastructure build out, and capital call risk.

Mid-to-late game = value creation, cash flow, often return of capital.

Late Game = exit

That orange line? It’s the J-curve—and it bends hard if the deal both “works” and is structured right.

Understand this curve, and you’ll understand the micro-cycle of the business. Often secondaries offer return of capital much sooner than investing in the beginning–this juices your internal rate of return to superior percentages even beyond investors that were there on day one.

Selectivity Wins

With secondaries you’re buying another’s time, business performance transparency, and proven market traction. The best investors treat them not as opportunistic scraps—but as a structured, cash-generating slice of their alternative stack.

It’s like picking cherries–be selective. ; )

HIDDEN GEM

Our Own Insider Access to 007 (Yes, That 007)

You probably know me for buying businesses—not making films. But what most don’t see is how similar those two worlds really are, and I apply the same thesis.

In both cases, I’m looking for the same thing: something proven that others overlook—an audience, a set of assets, or intellectual property that can be acquired, leveled up, and brought to market with a talented team.

In film, that translated to producing stories that premiered at Sundance (nominated for Best Documentary), SXSW (winner, Best Editing), and TIFF. I even earned an Emmy nomination in 2020. But most importantly? Every film I produced was acquired—usually by a streamer.

So, when Casper Daugaard approached me holding the James Bond license and a development deal with IO Interactive (the team behind Hitman), I was all in.

My father and I became the first investors in Delphi Interactive, back in February 2020. It remains one of the largest investments I’ve ever made—and we’re still one of the largest shareholders on the cap table.

A Secret Thesis Hiding in Plain Sight

Casper didn’t just have a license to one of the world’s strongest IP and the relationships in Copenhagen—a quiet powerhouse in game development thanks to studios like IO Interactive—to get it done, he also had a unique vision for how gaming will develop as an industry, and the opportunity that Delphi could capitalize on.

Everyone was trying to adapt games into movies. But what if you flipped the script?

“What if you took the world’s most beloved IP—film and TV—and built original AAA games around it?”

Not just “video games.” These aren’t phone apps. But rather, one of the most capital-intensive, IP-protected, hit-driven sectors of the entertainment world: AAA video games.

Enter Delphi Interactive. The thesis is simple but bold:

If you have world-class IP, independent talent, and capital — you don’t need a legacy publisher.

No EA. No Ubisoft. No Activision.

Just you, the IP, and the best developers in the world.

With the democratization of distribution, licensing franchise-able IP has become the core economic driver—not accessing the large legacy producers. Just like we’ve seen in tech, Casper saw there was an opportunity to build a 10-figure valuation with just a few people.

Breaking the Oligopoly

Delphi calls it the “publisher industrial complex.” Think old-guard AAA studios bloated with overhead and prioritizing their internal IP over yours.

What Delphi offers is radically different:

Beloved IP licensed directly from rights holders

Independent AAA studios like IO Interactive (makers of Hitman)

Financing and production support to deliver Hollywood-caliber games

Today, Delphi has a fully funded 007 video game and is considering release dates. It’s the first original James Bond story ever told in game form. Not tied to any film, not linked to any actor, just original, AAA narrative, drawing inspiration from the entire cannon.

And that’s just the beginning. Delphi’s pipeline for 2026 and beyond is impressive by any standard, further, the team Casper has assembled has built two gaming companies with $1B+ valuations.

What We’re Doing Now

Earlier this year, after launching Build Wealth, I approached Casper, asking if there was an opportunity I could create secondary access for our investors.

Because of my relationship and knowledge of both Delphi’s terms and waterfall, I was able to secure something rare:

A small, $1.4 million secondaries offering—with our investors in a first-out position, receiving capital back upon the game’s release.

Obviously, the raise filled in 10 days.

And just before sending this issue to print, I’m excited to share that we appear to be finalizing a second, and final, allocation of $1.5 million—on the exact same terms.

The updated fund paperwork and diligence are on track to being finalized next week.

If I’m lucky enough to bring this allocation to fruition, we do have investors who missed out last time lined up for this new allocation, so priority will go to them.

If you’re interested:

Review the opportunity, paperwork (being updated), understand fees & risks, and make a soft commit on our portal HERE.

If you have real interest, I’d encourage you to make a soft commitment, so I know who you are!

This has been an exciting deal and I’m thrilled to be able to extend this 5-year aged investment to our community.

-Walker

P.S. Here’s that link again.

CASE STUDY

What EQT’s Billion-Dollar Gaming Bet Reveals About Buying Smarter

In 2024, a quiet but monumental shift happened in the gaming industry—not in a flashy launch trailer or celebrity-packed keynote, but in a boardroom in Dublin.

Keywords Studios, the behind-the-scenes powerhouse supporting some of the world’s biggest video games—Fortnite, League of Legends, Call of Duty—agreed to a £2.2 billion buyout from private equity giant EQT.

Most players have never heard of Keywords. That’s the point.

They don’t make games. They make games better—handling localization, voice acting, testing, and development support for nearly every major studio on the planet. Think of them as the "AWS of gaming": invisible, essential, and everywhere.

So why does this matter?

Because this wasn’t just a big acquisition. It was a signal.

EQT didn’t get in early. They didn’t bet on a moonshot indie studio. They made a late-stage, secondary-style play: acquiring a mature, cash-flowing business embedded across the industry’s biggest titles.

In a market where IPOs are scarce and exits are elusive, they found a different way in: Buy quality. Mid-cycle. Hold long. Unlock value later.

EQT didn’t try to predict the next big thing. They didn’t back a new studio from scratch or speculate on a metaverse token. They acquired a mature, profitable, high-retention service provider embedded across the entire gaming industry.

If you’ve read Buy Then Build, you already know this playbook:

Buy proven performance, not potential.

Look for entrenched infrastructure, not just front-end flash.

Acquire cash flow, not pipe dreams.

And that’s exactly what EQT did.

This Is the Same DNA Behind Secondary Investing

While the EQT/Keywords deal wasn’t technically a secondary—it was a full buyout—it reflects the same investor psychology behind great secondary opportunities.

Because what makes a good secondary?

You’re not buying blind—you have data on what you’re stepping into.

You’re entering mid-cycle, where the risk has been de-risked and the value has been established.

You’re prioritizing cash flow and quality, not early-stage hype.

You get a shorter duration, a more defined exit horizon, and better clarity on return mechanics.

Sound familiar? It should. It’s Buy Then Build, applied to minority stakes and fund positions instead of businesses.

The best secondaries and the best acquisitions are both built on this shared truth:

Building on top of value that others have already built is the ultimate leverage.

Where LPs Should Be Watching

Private equity’s interest in gaming is baked on the trademarks of a sticky business model. It’s a high-retention, high-margin, IP-driven sector that throws off predictable cash flow once scaled.

And while a headline buyout like EQT’s is typically reserved for institutional capital, it points toward the next wave of opportunity for LPs–where they can access mature assets and gain enhanced liquidity options.

GP-led secondaries – A sponsor holding a valuable gaming asset wants more time or fresh capital, and rolls it into a continuation vehicle.

LP interest sales – A fund with heavy gaming exposure opens up a secondary window for existing LPs to sell their stakes.

Direct secondaries – Founders, employees, or early backers of gaming companies want liquidity—offering access to late-stage shares at a discount.

The mistake many investors make is thinking of secondaries as “leftovers.” But when executed well, secondaries—and acquisition entrepreneurship—are about the same thing:

Buying quality assets, with known performance, at the right time.

Late-stage, high-retention businesses in massive industries? That’s exactly where secondaries thrive.

In every maturing market—from software to healthcare to gaming—we’re going to see more of these: sponsors recapitalizing prized assets, rolling them forward, and inviting LPs into a new structure that offers real performance and shorter durations.

That’s not a backup plan. That’s just smart investing.

The bottom line? Whether you’re buying businesses or buying into funds, the best outcomes come from buying cash flow with clarity—not chasing optionality.

"The most dangerous thing in investing is assuming liquidity will always be there"

Michael Burry

Like this issue? Have an idea for a topic you’d like to see covered? Hit reply and share your thoughts. We read every single email.