Hi {{first_name}},

When headlines catch up to fundamentals, it’s already too late.

Oil prices are back in the news—surging on war headlines and geopolitical risk. But here’s the part no one’s saying out loud: oil was already mispriced before the first missile flew.

Global demand has been quietly climbing. U.S. supply has been quietly shrinking. And institutional capital? Still asleep on the sidelines.

This isn’t a blip—it’s a correction. The market is finally waking up to what the data has been saying for over a year: we’re staring down one of the most mispriced, cash-flowing real assets in the world.

U.S. wells decline ~7% annually

New drilling isn’t keeping up

Private equity investment is still down 60% from 2020

Demand? Up nearly 7x since early last year

And as of last week, the headlines are finally catching on.

Energy’s become ideological. But wealth gets built by focusing on cash flow, not headlines. Oil isn’t dead—it’s discounted. And right now, the smartest investors I know are leaning in, not out.

Inside this week’s issue:

• Why oil is the hidden yield asset in today’s Wealth Stack

• How Warburg Pincus turned a brutal energy cycle into outlier returns

• How to structure energy investments for asymmetric upside

This door won’t stay open forever.

Let’s walk through it.

Want alternative investing insights right in your inbox? Subscribe here!

SHIFT YOUR STACK

The Energy Asset Hiding in Plain Sight

Why smart investors are rushing into the most mispriced, cash-flowing real asset in the world

Oil prices are back in the headlines—spiking on news of war.

But that’s not the real story. The real story is what was already broken before the headlines hit.

For years, ESG mandates and institutional divestment have pushed capital away from oil and gas. But global demand hasn’t gone away—in fact, it’s still climbing. Meanwhile, supply has quietly eroded beneath the surface.

U.S. wells decline fast—over 20% in the first year, then around 6.5% annually. New drilling has failed to keep up. Since 2020, private equity investment in upstream oil & gas is down more than 60%. This isn’t a short-term supply squeeze. It’s a long-term dislocation that war just brought into focus.

In other words, the market wasn’t pricing oil correctly before. Now it’s being dragged back toward reality.

This is where sophisticated capital is stepping in.

The top 0.1% aren’t trading energy headlines—they’re owning energy cash flow. They’re not betting on volatility. They’re buying production. And they’re treating oil the same way institutions used to treat core real estate: a cash-flowing real asset with asymmetric upside and meaningful tax advantages.

In this week’s report, we dive into the data on our dwindling energy supply. Oil is still the most traded commodity on Earth. It’s essential. It’s cash flowing. And right now, it’s still mispriced.

Smart LPs aren’t asking, “Is oil dead?”

They’re asking, “What’s the smartest way to own it?”

CASE STUDY

How Warburg Pincus Turned an Energy Crash Into a Wealth Stack

The best investors don’t avoid cycles—they play them.

That’s exactly what Warburg Pincus did during the brutal 2016–2019 oil and gas downturn. While public markets panicked, they went to work—building a layered energy strategy that delivered returns traditional investors could only dream of.

Here’s how they turned a commodity crash into a compounding machine (*and how you can steal their playbook).

The Setup: Blood in the Oilfields

By early 2016, oil had collapsed from ~$100 to $26.

The ecosystem was on fire:

Shale producers were drowning in debt

Oilfield services were liquidating equipment

Banks were pulling back hard—capital was scarce

That’s the moment cycle-savvy investors move in. It’s when it feels contrarian.

Warburg’s Stack

Private Equity – Buy Distressed, Build Into Recovery

In 2017, Warburg seeded Ridge Runner II, a shale operator in the Delaware Basin.

$300M commitment

Strategy: Acquire discounted acreage, drill cheaply

Exit: Significant gains as oil rebounded

Private Credit – Lend Into the Panic

To fill the capital void, Warburg launched an energy credit fund.

Senior + mezzanine debt

Equity kickers for upside

Returns in the high teens to low 20s IRR

Hard Assets – Buy the Equipment Everyone Else Is Selling

They acquired oilfield services and offshore assets (e.g. Trident Energy) at distressed prices.

As activity returned, margins followed

Built asset exposure while others were running for the exits

The Takeaway: Observe, and Play, the Cycle

Warburg didn’t “time the market.” They observed the cycle.

And they played accordingly:

Buy real assets when distressed

Lend when capital is scarce

Own what others fear

That’s how intelligent wealth is built. The smartest capital doesn’t follow headlines—it follows the cycle. And it knows how to structure for upside when others are uncertain.

Wall Street missed it then. They’re missing it again now.

The pricing is off. The positioning is light.

Let’s dive into what the fundamentals are telling us today…

BEHIND THE NUMBERS

The Institutional Blind Spot Hiding in the Oil Market

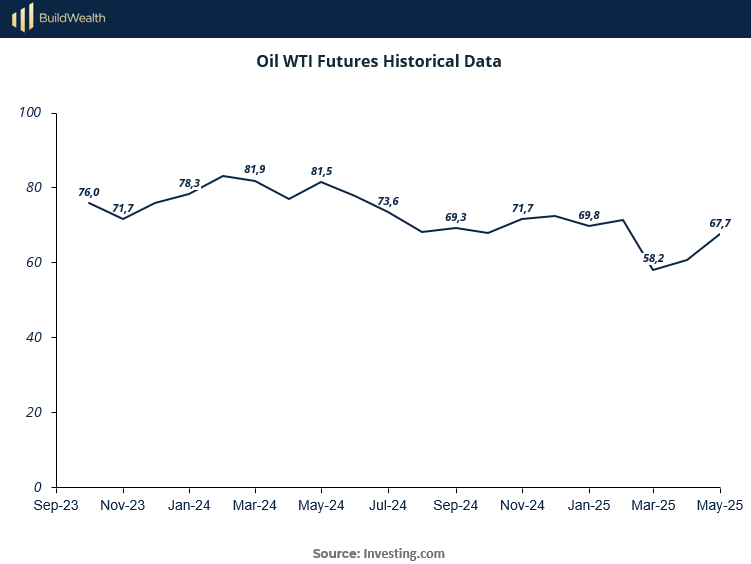

On paper, oil looks stable. Futures are flat. And while headlines are flashing bullish on geopolitical tension, the market still hasn’t caught up to the bigger story: the fundamentals are broken—and almost no one is pricing them in.

Empirical evidence suggests we’re headed toward a mid-term energy supply squeeze—driven not by speculation, but by years of underinvestment. Inventories are tight. Capex is still below trend. Demand isn’t slowing. And most allocators haven’t repositioned. That kind of gap between market behavior and physical reality? It’s where private markets allow for capitalizing on inefficiencies.

Where We Actually Are in the Cycle

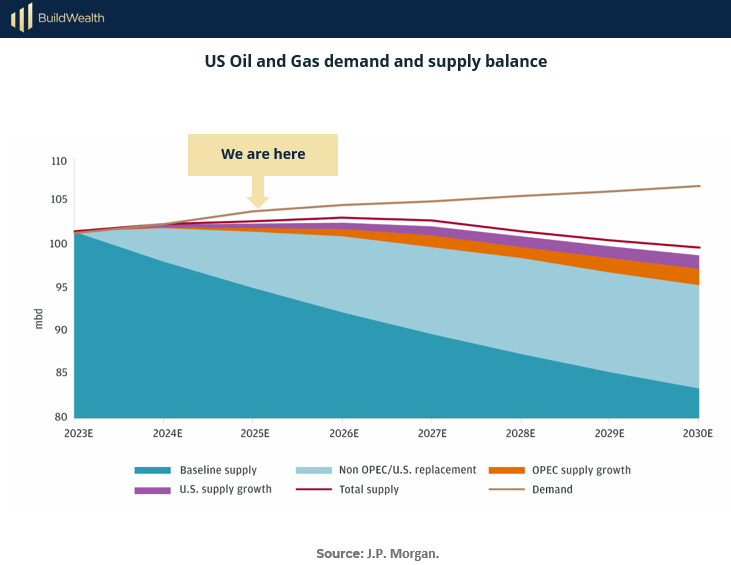

This isn’t 2020 anymore. We’re in Wave 3 of the energy supercycle—where falling inventories, declining investment, and steady global demand quietly reset the floor.

But most of the market is stuck in Wave 2 psychology: still anchored to post-COVID softness, assuming supply will magically rebound. It won’t. And the data is hiding in plain sight:

The Market’s Mispricing Is Visible

Even though we’re entering a supply-constrained era, the market isn’t fully pricing it in.

You can see this disconnect in the current WTI futures curve—prices drift lower into 2025, implying soft demand and adequate supply. But fundamentals tell a different story:

WTI futures still imply lower prices through 2025

OPEC+ cuts remain in force

Inventories are below 5-year averages

Global upstream capex is far below 2010s levels

China’s demand is picking back up

Private capital still hasn’t returned in force

As J.P. Morgan’s Christyan Malek recently put it:

"We are turning bullish now as we envisage an emerging supply-demand gap beyond 2025."

That’s not a trade. That’s a thesis.

Why It Matters for LPs

The window we’re in right now is classic: a mispriced real asset with strong cash flow, inflation protection, and limited competition for deals.

Public sentiment hasn’t caught up. The forward curve is still asleep. And institutional capital is underexposed. That gives private LPs a unique advantage—access to yield-rich energy assets at entry points the rest of the market will only recognize in hindsight.

Price and value are diverging. That's historically when you want to be a “contrarian” investor.

THE PLAYBOOK

Two Proven Paths to Invest in Oil & Gas—Which One Fits Your Goals?

There’s more than one way to invest in energy. The question isn’t which strategy is “better.” The question is: What’s your goal?

Here’s how the two most common approaches break down:

1. The Active Income Tax Saving Strategy

Designed for large first-year write-offs

If your primary goal is to offset active income—especially W-2 income—this strategy is built around maximizing deductions.

Focuses on new drilling with limited or no production at the start

Generates significant first-year write-offs through intangible drilling costs (IDCs)

May allow for active income offsets if structured properly

Comes with higher risk: undeveloped acreage, binary outcomes, drilling execution risk

Often used by high-income professionals seeking short-term tax relief

Oil & gas is the only asset class where you can write off 70–90% of your investment against your W-2 income in year one — without quitting your job. It’s a legitimate approach—but it’s best suited for investors who are primarily optimizing for taxes (and tend to lean towards more drilling risk). Important: GP investments come with personal liability, so due diligence is critical.

2. The “Cash Flow + Build” Strategy

Structured for compounding yield and long-term value

If your focus is on durable cash flow, strategic appreciation, and a tax advantage that trails the economics—not drives them—this is the model to study.

Acquires existing, cash-flowing wells with proven reserves

Infill drilling boosts production over time with lower risk

Income begins early and compounds as production grows

Still benefits from IDCs and depletion allowance—but without speculative drilling

Targets mid-20s IRRs with downside protection and strong operator control

This is the model favored by institutional LPs, family offices, and investors who play the cycle—not just the tax code. They want exposure to hard assets, real yield, and structural upside—not operator risk and binary outcomes.

This is supported by three fundamental approaches:

1. Institutional Allocation Trends Favor Proved Developed Producing (PDP) and Yield-First (i.e. actively cash flowing) Strategies

2. Family Offices Avoid Operational Complexity and Binary Outcomes (i.e. non-working interest and avoiding the “lottery” of exploration).

3. Investors “playing the cycle" prefer undervalued cash flow, not binary risk (i.e. the old “buy low, sell high” lesson).

Five Questions to Ask Before Writing a Check into an Oil Deal

Is the well already producing—or just a map with a plan?

What’s the operator’s track record across multiple price cycles?

How is production expected to grow over time—exploration or infill?

Are the tax benefits clearly documented and compliant?

Am I investing for real yield—or chasing a deduction?

What We’re Doing at BuildEnergy Fund I

With BuildEnergy Fund I, we’ve structured our fund around the second model:

We acquire existing production, enhance value through low-risk infill drilling, and partner with a GP team that’s delivered 30%+ IRRs over four decades—including a 36% IRR in their most recent fund.

It’s a buy-then-build strategy in energy—built for LPs who want cash flow, tax efficiency, and asymmetric upside in a supply-constrained market.

Curious how we’re applying this strategy right now?

Take a look at BuildEnergy Fund I or check out the full Deal Drop HERE.

You’ll see exactly how we’re positioning capital through the cycle.

WEALTH STACK TOOLBOX

Financial Metrics Toolbox for Oil & Gas Investors

If you want to play in the Oil & Gas space, here’s the first rule: you need to speak the language of capital. That language? Financial metrics.

Unfortunately, too many private investors get seduced by “high yield” stories or “insider” deal flow without understanding how to rigorously evaluate these opportunities. The result? They end up owning a royalty stream that doesn’t pay, or a WI (working interest) stake with hidden capex bombs.

That’s why I’m spotlighting this Financial Metrics Toolbox — a simple but powerful Excel-based toolkit that lets you calculate and sanity-check the metrics that actually matter in upstream and midstream Oil & Gas deals.

Why It’s Useful:

Oil & Gas isn’t your typical SaaS or HVAC acquisition. You’re dealing with decline curves, PDP vs. PUD reserves, and multiple layers of risk: operational, commodity price, and regulatory. Having a clear view of financial performance, leverage, and capital efficiency is non-negotiable.

Key Metrics You Can Model:

Operating costs per BOE

Netback margins — are your lifting costs low, high or moderate

F&D costs per BOE - How efficiently are you converting capital into new reserves?

Profitability ratios

Efficiency ratios

Who It’s For:

Accredited investors writing checks into mineral rights, royalty funds, or direct WI deals

Operators seeking to evaluate acquisition targets

Family offices looking to move beyond public MLP exposure

Bottom Line:

In Oil & Gas, you don’t get paid for stories — you get paid for barrels. This toolbox helps cut through marketing fluff and puts math back in the driver’s seat.

THE MINDSET SHIFT

Most investors still think about oil like it’s a bet—on price, on politics, on global chaos. But the smart money doesn’t see it that way. They’re not trading futures—they’re buying production. They’re owning real assets with durable yield, inflation protection, tax benefits, and structural tailwinds the public markets haven’t priced in yet.

The shift? Stop reacting to the headlines—and start positioning ahead of them.

Because cycles don’t punish prepared capital. They reward it.

Want to see how we’re investing through the cycle?

$50,000 minimum, accredited investors only.

WHAT WE ARE READING

"In the short run, the market is a voting machine. In the long run, it is a weighing machine."

Benjamin Graham