Hi {{first_name}},

We’re in a new era of lending.

Banks have pulled back. Bonds are underperforming. But private credit? It’s booming.

In the last decade, it’s grown from $500 billion to $2.1 trillion—and McKinsey thinks we’re headed for $30 trillion. That’s not a trend. That’s a global reset.

And here’s the kicker:

You’re not betting on growth. You’re lending against it.

That’s what makes private credit so powerful right now.

You're not chasing alpha. You're underwriting cash flow. You're not hoping for an exit—you’re getting paid along the way.

This is the same mindset that built my career acquiring businesses with real cash flow, real assets, and real upside. Buy what’s already working. Then structure for control, yield, and downside protection.

At Build Wealth, we’re not chasing headlines. We’re aligning with this structural shift. Every dollar you invest is placed with rigor—I’m structuring deals with operators I know, then completing extensive diligence and investing my own money. The goal is to stack returns in our investors’ favor–beyond what any of us could get on our own.

Maybe this is why we’re outpacing every private capital raiser.

We’re not chasing yield.

We’re engineering it.

Inside this week’s issue:

Why private credit is posting bond-beating returns with real downside protection

A behind-the-scenes look at a deal we structured for a 14% secured return (and why the borrower begged us to do it)

Our 6-step LP Playbook for vetting credit funds like a pro

And a downloadable Private Credit Scorecard to help you diligence any deal like an insider

It’s private credit, with the entrepreneur’s edge. ; )

SHIFT YOUR STACK

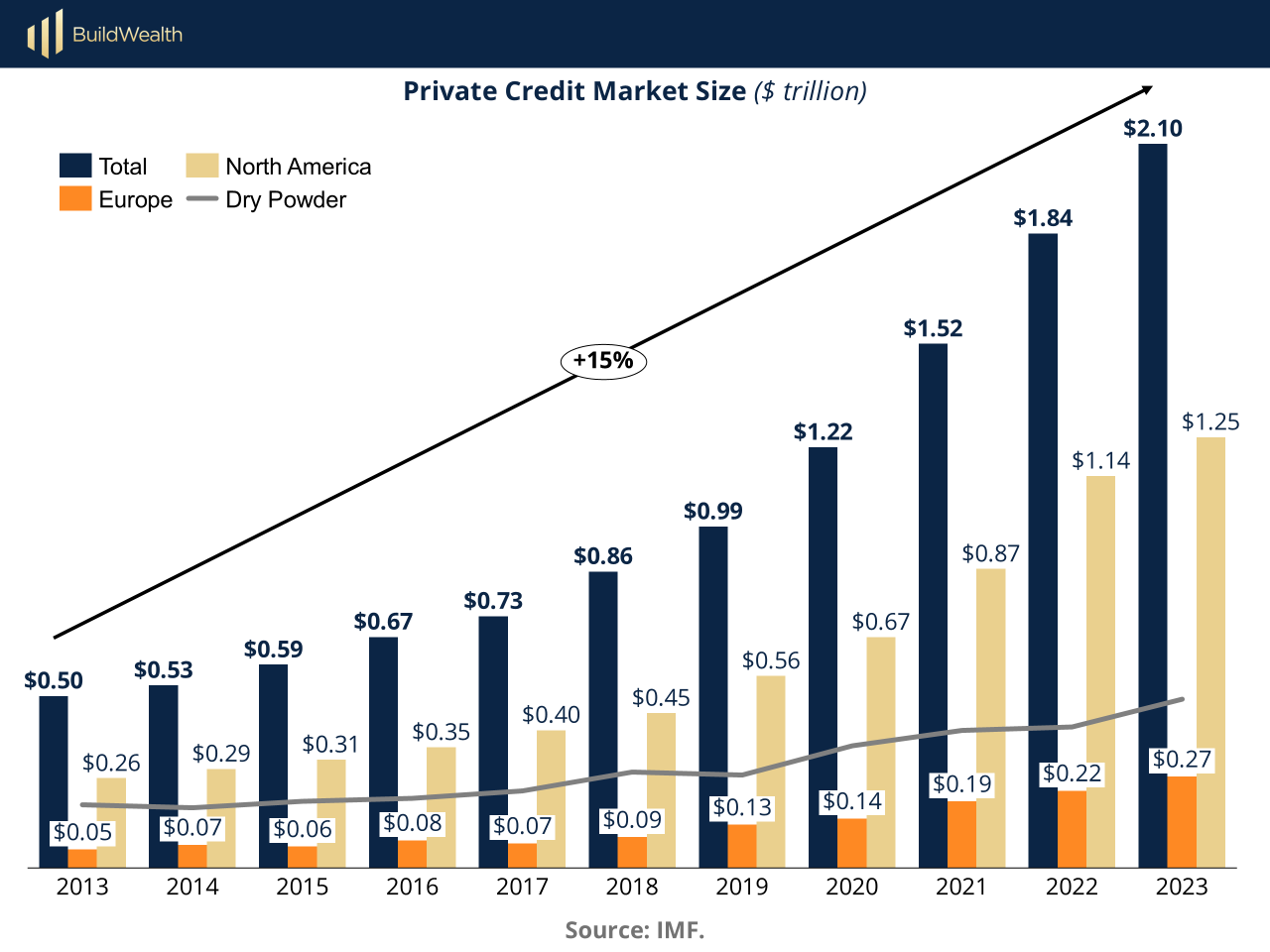

Private Credit: The New $2.1 Trillion King of Yield

(Or Why Smart Money is Rotating Into Bespoke Lending)

Can we all agree the 60/40 portfolio doesn’t work anymore? It underperforms.

Rising rates broke the yield curve. Bonds aren’t delivering. And banks? They’ve retreated from lending. Meanwhile, private credit has stepped in—not just as a replacement, but as a structurally superior asset class. Private credit is exploding.

Ten years ago, the private credit market sat at $500 billion. Today? It’s over $2.1 trillion and growing at a 15% annual clip. McKinsey projects the market could hit $30+ trillion over the next decade. Right now, we’re only at $2 trillion.

That’s like getting in on real estate in the ‘80s or tech in the late ‘90s.

The market is expanding because a systemic bank retrenchment is allowing for:

Companies need faster, more flexible financing.

Traditional banks are throttled by regulation.

Investors want yield with protection—and private credit delivers.

This isn’t a trend—it’s a full-blown rewire of the global credit system.

So what makes private credit different?

Equity-like returns with lower loss rates

Private credit averages just 0.9% in annual loss rates, outperforming high-yield bonds—and without the daily volatility of public markets.

Returns that rise with rates

Most private credit loans are floating rate. So when the Fed hikes, your returns go up. Between 2008 and 2023, direct lending delivered an average return of 11.6% across rate hikes.

Stress-tested performance

During COVID, private credit posted a drawdown of just -1.1%, outperforming leveraged loans and high-yield debt.

Full-stack control

These aren’t passive bond investments. Deals are structured with covenants, collateral, and often personal guarantees. You’re not buying paper—you’re buying protection.

Follow the Smart Money

Apollo raised $50B+ in private credit last year. Ares, Oaktree, KKR—they’ve gone all-in. They’re not betting on the bond market coming back. They’re building the next one.

BEHIND THE NUMBERS

Why Secured Loans Are the Backbone of Smart Private Credit Investing

Let’s get one thing out of the way: "credit fund" is a catch-all term that gets thrown around a lot. But not all credit is created equal.

Some funds are lending against hard assets. Others are underwriting optimism. Some sit at the top of the capital stack with first-lien protections. Others are one bad quarter away from a total write-off.

When I tell people that our private credit fund only lends on secured loans, they usually nod politely. But I can tell most don’t fully grasp how important that detail is.

Let me put it this way: If you're going to lend someone your money, would you rather have a handshake—or a handshake and a lien on their house?

That’s collateral. And it’s the backbone of how we protect capital in a volatile world.

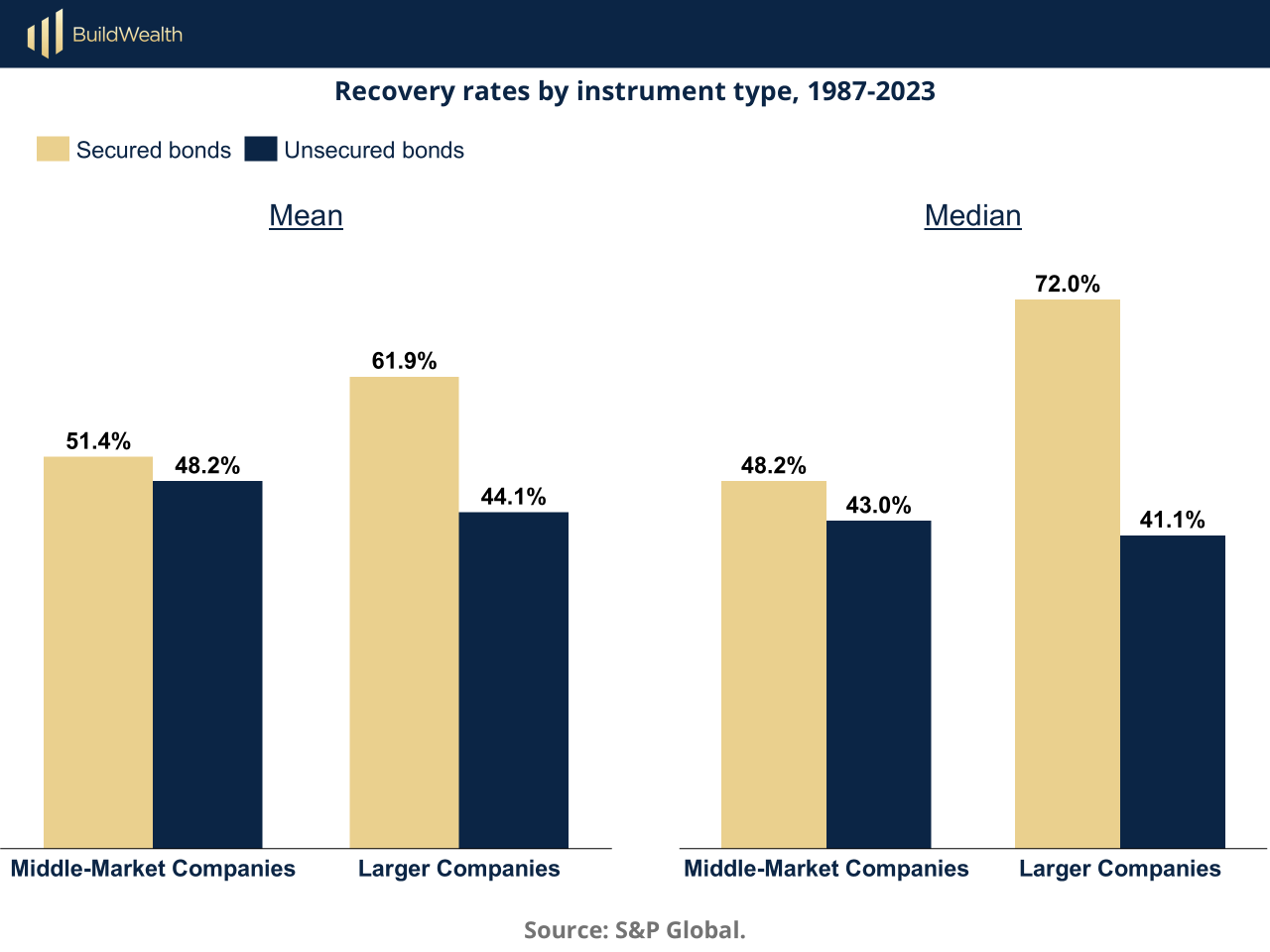

A new working paper from the Bank for International Settlements puts numbers behind what we already know: secured lending is booming. Outstanding secured loans have shot up to $370 billion—now making up more than half of all direct lending. And here’s the kicker: these loans often come with higher spreads and longer maturities than unsecured loans. Translation? You get paid more to take less downside risk.

Why? Because as lenders move further away from borrowers—both literally and figuratively—we rely more on collateral to bridge the information gap. Think of it as trust with a seatbelt.

If you want real downside protection, you need more than just assets on paper. You need position, control, and priority. And that’s exactly how we build our fund.

Here’s our structure at Build Wealth, in plain English:

(Over)Collateralized – Every dollar we lend is backed by real assets—often at loan-to-cost ratios below 65%. We’re not taking equity risk and hoping for the best. We’re lending against the part of the deal that already works.

Preferred Position – We target mezzanine and preferred equity positions that sit ahead of common equity and often in front of outside LP capital. It’s not just about yield—it’s about getting paid before anyone else does.

Control Rights – This is the game-changer. Our deals are structured with operating agreement control, second-position authority, and forced sale provisions. We don’t just hold paper—we hold the keys.

In a world where everyone’s chasing double-digit yield, the real flex is building a position that actually gets repaid if things go sideways.

And that’s not theory. That’s structure.

Every asset we lend against is vetted, valued, and underwritten by a team that’s structured over $4 billion in deals. That’s not theory—it’s track record; and we make it available to everyday accredited investors with a $50k minimum investment.

This is what we mean when we say we’re engineering yield—not chasing it. Our credit deals don’t live at the mercy of market timing or interest rates. They’re stacked with protections, priced for volatility, and structured to move fast when others can’t.

So yes—collateral matters. But by itself? It’s a seatbelt.

What we build is the whole roll cage.

So that’s why I’m up to my ears in debt. ; )

CASE STUDY

Why a Borrower Paid 14% Interest to Our Credit Fund (Instead of Going to a Bank)

Last year, we closed a credit deal in our own credit fund (BuildFlow I) that checks all the boxes: prime location, value-add upside, assumable cheap debt—and a preferred equity layer that delivers double-digit returns with senior-level security.

The deal? A 100+ unit multifamily property in Lee’s Summit, one of the fastest-growing submarkets in Kansas City. Surrounded by new Class A development, this property sits right in the path of progress. It’s a classic value-add play—think deferred maintenance, outdated interiors, and operational upside. But here’s where it gets interesting.

The operator secured the property with a Freddie Mac assumable loan at 2.94% interest. There were three years remaining on the term when it went under contract. Problem was, that debt only covered 45% of the total acquisition cost. That left a big hole in the capital stack—and they weren’t interested in blowing up the deal by refinancing into a 7% bank loan.

So… Why Not Just Go to a Bank?

Simple. A bank wouldn’t let them keep the cheap Freddie debt. And a bank certainly wouldn’t lend in second position. So replacing that 2.94% loan with new senior debt at market rates would’ve crushed the economics—and likely killed the deal. Enter us.

We stepped in as the preferred equity provider with a $1.5M position that sits in front of the common equity but beneath the senior. Our structure was designed to blend into the capital stack without compromising it:

8% current pay, monthly

6% accrued and compounding monthly

2% origination fee

No principal payments during the hold

On paper, that’s a 14% total return. But in reality, the borrower is only paying 8% today—and happily so. Why?

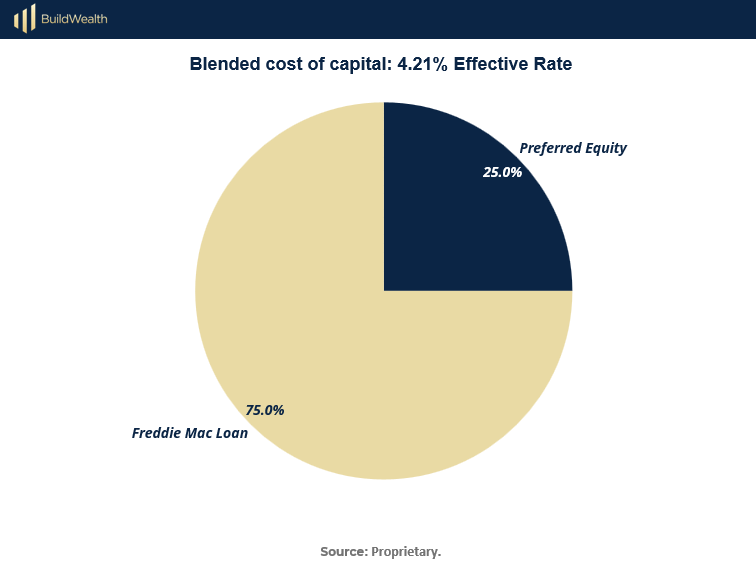

Because 75% of their total capital is costing them less than 3%. Our 15% pref piece costs 8% monthly. When you blend it all together, their effective cost of capital sits closer to 4.21%. That’s lower than any bank loan they could get—and it gives them flexibility to execute their business plan without over-leveraging.

But Wait… With 4.2% debt, Why Not Just Be an LP?

It’s a fair consideration. The common equity investors on this deal will likely do great. But they’re in the riskiest seat—last to get paid, no guarantees, and entirely dependent on execution and market timing.

By contrast, we have collateral. We have rights. We have control.

Because we’re approved by Freddie, we were able to be written into the deal with full second-position authority—something most lenders can’t get. We were added to the operating agreement itself, giving us the right to force a sale if things go sideways. This isn’t theoretical, it’s real downside protection.

Even in a distressed scenario, we sit behind a Freddie loan and ahead of the equity. With a combined 60% loan-to-cost, that gives us a built-in 40% equity cushion. In other words, the property value would have to drop by nearly half before we’d lose a dime.

It’s the kind of asymmetric profile we aim for again and again:

Low downside. Low volatility. Predictable income. Compounding, equity-like upside.

And that’s why these structured credit deals are becoming a cornerstone of my own strategy (I’m currently tied in first place as “largest investor” in my own credit fund).

Want a portfolio of deals like this?

Our credit fund currently holds a portfolio of 8 similar loans in it and we have executed term sheets on 2 more… and our pipeline is full (our team reviewed over 1,000 potential loans to pick these 10). We target returns of 12–14% with low volatility and real collateral protection.

You can review the BuildFlow I deal drop and offering docs here: https://buildwealth.investnext.com/

THE PLAYBOOK

The LP Playbook: How to Vet (and Win With) Private Credit

Private credit is booming—and for good reason. But the biggest mistake new LPs make? They chase yield without understanding the structure. Not all credit deals are created equal. In fact, many credit deals out there are misguided equity plays.

Smart investors treat every credit fund like an underwritten deal.

Here’s your step-by-step playbook for evaluating private credit like a next-gen LP.

Step 1: Know Why You’re Here

Every allocation you make should have a purpose. Is this capital meant to offset volatility, produce income, or diversify away from public market risk?

Know what you’re solving for before you diligence a single deal. There are reasons to invest in the equity side of things (asymmetrical return), and reasons to invest in the debt side of things. Be clear about your goals while building your wealth stack so you can allocate appropriately.

(Want to consult with our team about that? Schedule a call with us here. We love alts, but we love diversification more.)

Step 2. Underwrite the Manager First

Before you evaluate deals, evaluate the people creating them.

Ask:

Who’s originating and underwriting?

Have they operated through a downturn?

Do they have a sourcing advantage—or are they buying someone else’s scraps?

Look for:

Repeatable sourcing and underwriting engine

Skin in the game (co-invest)

Process for monitoring covenants and restructuring underperformance

Track record of recoveries, not just originations

The fund’s alpha isn’t in the yield. It’s in the underwriting machine.

Step 3: Understand the Strategy (and Your Place in the Stack)

Private credit lives above equity in the capital stack — which means less upside, but also less downside. You're the lender, not an owner.

But that doesn't mean you're always first in line either. Not all credit is created equal. Some credit funds take senior-secured positions. Others are mezzanine lenders taking subordinated risk.

Are you in senior secured, mezzanine, or unitranche? Is this a bridge to a sale, an acquisition loan, or structured growth capital?

Ask:

What’s the loan-to-value (LTV) or loan-to-enterprise value (LEV)?

Is the loan asset-backed, cash-flow based, or personally guaranteed?

Is the risk/reward appropriate for the layer of the capital stack you’re in?

The higher you sit in the capital stack, the lower the risk—and the more your principal is protected.

4. Follow the Flow of Capital and Incentives

The most overlooked part of any fund: incentives.

Ask:

Is yield generated through interest payments—or juiced by equity kickers and exit fees?

Are borrowers actually paying—or are returns being smoothed by internal bridge funding?

Are fees based on committed, deployed, or NAV-adjusted capital?

And don’t forget the sponsor alignment:

Is there a preferred return before carry?

How much of their own money is in the fund?

Pro Tip: If the manager isn’t aligned with you economically, you’re the yield.

5. Map Liquidity and Duration (Don’t Get Trapped)

Direct lending funds are commonly semi-liquid, not illiquid. Know how and when you get your capital back.

Ask:

What’s the average loan duration?

Are distributions monthly or quarterly, or rolled until maturity?

After the lockup period, what are the redemption terms? (90-day notice? Sponsor discretion?)

Illiquidity shouldn’t be the risk, it should add to the return.

6. Stress-Test the Return

A 12% yield looks great—until you realize it’s not being paid in cash or it’s backed by a shaky borrower.

Ask:

What’s the real cash yield vs. the paper yield?

What’s the default rate? The recovery rate?

What’s the downside scenario, and how does the sponsor handle distress?

7. Creditors Have Control

Lenders typically have power. The right to foreclose, force a sale, restructure terms, and protect your downside.

Passive income shouldn’t mean passive positioning. Great credit investors often engineer a ripcord. What’s yours?

Think Like a Lender

Private credit isn’t about chasing the highest number. It’s about buying disciplined, repeatable cash flow, with downside protection baked in. This almost completely eliminates volatility.

Sophisticated LPs don’t just ask, “What’s the yield?”

Instead, we determine, “What’s the risk-adjusted yield, and who’s standing behind it?” We chase asymmetric risk-adjusted yield, backed by collateral, clarity, and control.

Private credit isn’t about getting rich fast. It’s about not losing money slowly.

And when done right? It can be the steadiest compounding engine in your entire stack.

WEALTH STACK TOOLBOX

Private Credit Due Diligence Scorecard

→ [Get the Template]

This one-page scorecard will force you to think like a credit committee.. It’s not about complexity—it’s about clarity. Fast.

You’ll drop in your responses to 40+ targeted diligence prompts—from revenue quality to lien enforceability—and it’ll score the deal across key risk domains. Every checkbox is tied to a red flag you’ll want to avoid.

Use It To:

Gut-check a borrower before digging into documents

Score deals against a common credit standard

Spot where risk may be hiding

Share a clear summary with partners or LPs

Private credit is a powerful asset leveraged by the ultra rich. And when done right it’s the steadiest compounding engine in your entire wealth stack.

WHAT WE’RE READING

"In private credit, the key isn't just finding yield—it's understanding structure. Good documentation and covenants are how you get paid back when things go wrong."

Howard Marks